%20(1).png)

Behind every successful online transaction sits a financial entity that most business owners have never consciously thought about, despite depending on it entirely to receive revenue. That entity is the payment acquirer and understanding what it does is one of the most practically useful pieces of payment infrastructure knowledge any ecommerce operator can have.

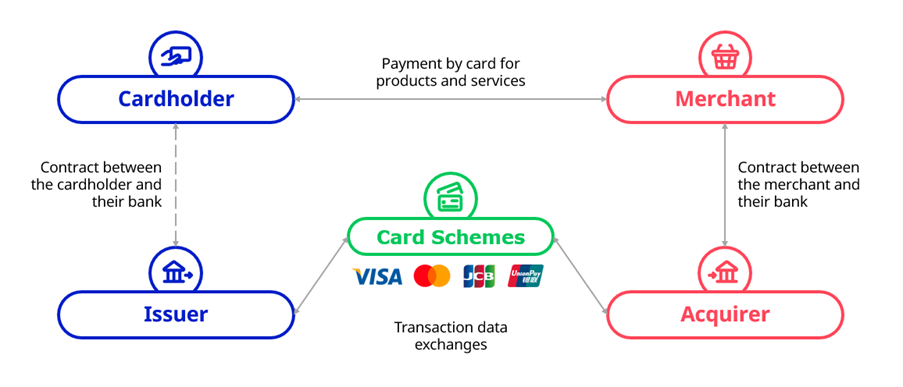

In simple terms, a payment acquirer also called an acquiring bank is the financial institution that processes card transactions on behalf of a merchant. It holds your merchant account, communicates with card networks like Visa and Mastercard on your behalf, and receives funds from your customers' issuing banks before settling them into your account. Without an acquiring relationship either direct or through a Payment Service Provider that aggregates acquiring infrastructure you cannot accept card payments at all.

The acquiring relationship directly influences your transaction acceptance rates, your settlement speed, your chargeback management, and ultimately how much of every sale you actually keep after fees. It is not a passive infrastructure component it is a commercially significant relationship that determines the financial performance of your payment stack from the first transaction to the millionth.

How Does a Payment Acquirer Work?

The payment acquirer operates at the center of every card transaction connecting your merchant account to the card networks and issuing banks that hold your customers' funds. Understanding exactly what happens at each stage of that process reveals why the acquiring relationship has such a direct impact on transaction costs, acceptance rates, and settlement speed.

The Authorization Process

When a customer enters their card details on your checkout and clicks pay, the payment data travels from your checkout through your payment gateway or PSP to your acquiring bank. The acquirer forwards the transaction details to the relevant card network Visa, Mastercard, or whichever network issued the card which routes the authorization request to the customer's issuing bank.

The issuing bank evaluates the request checking available funds, validating card details, screening for fraud signals, and applying its own risk assessment before returning an approval or decline decision through the card network back to your acquirer. Your acquirer relays that decision to your checkout in real time. The entire authorization sequence completes in two to three seconds from the customer's perspective but involves four distinct financial entities communicating in sequence.

The quality of your acquiring relationship directly influences this outcome. Acquirers with stronger card network relationships and more sophisticated authorization routing consistently achieve higher approval rates on the same transactions that weaker acquiring infrastructure would decline which is why acceptance rate differences between payment providers are fundamentally differences in acquiring quality rather than gateway technology.

The Capture and Settlement Process

Authorization confirms that funds are available but settlement is the process that actually moves money from the customer's issuing bank to your merchant account. Your acquirer manages this settlement process collecting authorized funds from issuing banks through the card network clearing system and depositing the net amount after deducting interchange fees, scheme fees, and acquirer margin into your merchant account.

Settlement typically occurs one to two business days after the transaction though the exact timeline depends on your acquirer, your merchant account type, and the card network involved. Acquirers with more efficient settlement infrastructure deliver faster access to funds and for businesses where cash flow timing is commercially significant, settlement speed is a meaningful dimension of acquiring quality that deserves evaluation alongside transaction fees.

Chargeback Management

When a customer disputes a transaction with their issuing bank, the chargeback process flows back through the same acquiring infrastructure in reverse. The issuing bank notifies the card network, which notifies your acquirer, which debits your merchant account for the disputed amount and presents the chargeback to you for response.

Your acquirer's role in chargeback management the quality of their dispute handling process, the evidence submission tools they provide, and the advocacy they exercise on your behalf with card networks directly influences your chargeback win rate and the net financial impact of disputes on your business. Acquirers with stronger chargeback management infrastructure consistently deliver better dispute outcomes than those with generic, minimal dispute handling processes.

What Is the Difference Between a Payment Acquirer and a Payment Processor?

These two terms are used interchangeably so frequently that the distinction between them has become genuinely unclear for most business owners and that clarity matters because the acquiring relationship and the processing relationship serve different functions in your payment infrastructure and carry different commercial implications.

A payment acquirer is a licensed financial institution a bank that holds your merchant account, maintains the formal relationship with card networks like Visa and Mastercard on your behalf, and is legally and financially responsible for the transactions processed through that merchant account. The acquirer is the entity that settles funds from issuing banks into your account, manages your chargeback liability exposure, and maintains the banking relationship that makes card acceptance possible. You cannot accept Visa or Mastercard payments without an acquiring bank sponsoring your merchant account within the card network system.

A payment processor is the technology layer that handles the technical execution of the transaction routing authorization requests between your checkout, the card networks, and the issuing bank, and communicating the approval or decline decision back to your customer in real time. The processor is a technology service rather than a financial institution it does not hold a merchant account, does not settle funds, and does not carry the regulatory and financial obligations of an acquiring bank.

In practice, this distinction has become less visible to most merchants because Payment Service Providers like Stripe, PayPal, and InflowPay bundle both functions providing processing technology and acquiring infrastructure through a single integrated service. When you sign up with a PSP, you are accessing their acquiring relationship rather than establishing a direct one with an acquiring bank which simplifies the infrastructure significantly but means that the acquiring relationship and its associated terms are managed by the PSP rather than negotiated directly with a bank.

The commercial implication is straightforward: the acquiring quality embedded in your PSP's infrastructure the banking relationships, the card network standing, and the authorization routing sophistication directly determines your acceptance rates, your settlement speed, and your chargeback management quality, regardless of whether you ever interact with the acquiring bank directly.

How Does a Payment Acquirer Affect Your Transaction Costs?

The acquiring relationship is one of the most direct determinants of what you actually pay to process payments and understanding exactly which cost components flow from the acquirer helps you evaluate payment infrastructure decisions with the commercial precision they deserve.

Interchange fees are the largest component of most merchants' payment processing costs and while they are set by card networks rather than acquirers, it is your acquirer that collects them on the card network's behalf and passes them through to your merchant account. The acquirer's ability to optimize interchange qualification ensuring that transactions qualify for the lowest applicable interchange tier based on the data submitted directly influences how much interchange your business pays per transaction. Acquirers with more sophisticated interchange optimization submit richer transaction data that qualifies more transactions for preferred rates producing a lower effective interchange cost without changing the card network's published fee schedule.

Acquirer margin is the fee the acquiring bank charges on top of interchange and card network scheme fees for providing the merchant account and settlement infrastructure. This margin varies between acquirers and is the most directly negotiable component of your payment processing cost particularly at higher transaction volumes where the acquirer's commercial incentive to retain your account creates pricing flexibility that smaller merchants cannot access.

Settlement timing affects your cost of capital rather than your direct transaction fees but for businesses where cash flow timing is commercially significant, the difference between a one-day settlement cycle and a three-day cycle represents a meaningful difference in working capital efficiency. Acquirers with more efficient settlement infrastructure deliver faster access to funds and at high transaction volumes, faster settlement has a quantifiable financial value that belongs in the total cost of ownership calculation.

Reserve requirements represent another acquirer-driven cost that most merchants underestimate. Acquirers managing their own chargeback exposure may hold a percentage of your transaction volume in reserve effectively removing that capital from your available funds for the duration of the reserve period. InflowPay's non-custodial infrastructure eliminates reserve risk entirely guaranteeing your funds remain fully accessible without the capital cost that reserve requirements impose.

Payment Acquirer FAQ

What is a payment acquirer in simple terms?

A payment acquirer also called an acquiring bank or merchant acquirer is the financial institution that processes card transactions on behalf of a merchant. It holds your merchant account, communicates with card networks like Visa and Mastercard on your behalf, and receives funds from your customers' issuing banks before settling them into your account. Without an acquiring relationship either direct or through a Payment Service Provider that aggregates acquiring infrastructure you cannot accept card payments at all.

What is the difference between a payment acquirer and an issuing bank?

An issuing bank is the financial institution that issued your customer's credit or debit card and holds their funds. An acquiring bank is the financial institution that holds your merchant account and receives funds on your behalf. When a customer makes a purchase, their issuing bank approves or declines the transaction and releases the funds through the card network and your acquiring bank receives those funds and settles them into your merchant account. The two banks are on opposite sides of every card transaction.

Do I need a direct relationship with an acquiring bank?

Not necessarily and most businesses do not have one. When you sign up with a Payment Service Provider like Stripe, PayPal, or InflowPay, you are accessing their acquiring relationship rather than establishing a direct one with an acquiring bank. The PSP manages the acquiring infrastructure on your behalf simplifying the setup significantly while embedding the acquiring quality of their banking relationships into your payment stack. Direct acquiring relationships are typically reserved for businesses at very high transaction volumes where the economics of direct acquiring justify the complexity.

How does my acquiring bank affect my payment acceptance rates?

Your acquiring bank's card network relationships, authorization routing sophistication, and banking infrastructure directly influence how many of your payment attempts succeed. Acquirers with stronger card network standing and more sophisticated routing consistently achieve higher approval rates on the same transactions that weaker acquiring infrastructure would decline. This is why acceptance rate differences between Payment Service Providers are fundamentally differences in acquiring quality and why InflowPay's industry-leading acceptance rates reflect the strength of the acquiring infrastructure embedded in its payment stack.

What is interchange and how does my acquirer affect what I pay?

Interchange is the fee paid to the customer's issuing bank on every card transaction set by card networks and representing the largest component of most merchants' processing costs. Your acquirer collects interchange on the card network's behalf and passes it through to your account. Acquirers with more sophisticated interchange optimization submit richer transaction data that qualifies more transactions for lower interchange tiers reducing your effective interchange cost without any change to the card network's published fee schedule.

What is an acquiring reserve and how does it affect my business?

An acquiring reserve is a percentage of your transaction volume that your acquirer holds back typically in an escrow or reserve account as financial protection against chargeback losses. Reserve requirements reduce your available working capital for the duration of the reserve period and represent a real financial cost that most merchants do not include in their payment infrastructure cost calculations. InflowPay's non-custodial infrastructure eliminates reserve risk entirely guaranteeing your funds remain fully accessible without the capital cost that reserve requirements impose on merchants using custodial acquiring infrastructure.

How does a payment acquirer handle chargebacks?

When a customer disputes a transaction with their issuing bank, the chargeback process flows back through the acquiring infrastructure. The issuing bank notifies the card network, which notifies your acquirer, which debits your merchant account for the disputed amount and presents the chargeback to you for response. Your acquirer's chargeback management quality the dispute handling tools they provide, the evidence submission process they support, and the advocacy they exercise on your behalf with card networks directly influences your chargeback win rate and the net financial impact of disputes on your business.

What is the difference between a direct acquiring relationship and an aggregated one?

A direct acquiring relationship means your business has its own merchant account with an acquiring bank negotiated directly, with your own pricing terms and your own card network standing. An aggregated acquiring relationship means you process payments through a PSP that maintains a master merchant account with an acquirer and aggregates multiple merchants under that account. Direct acquiring offers more pricing control and higher transaction limits at very high volumes but requires the financial history, transaction volume, and compliance infrastructure that most early and mid-stage businesses have not yet established.