How To Choose a Payment Processor?

Every ecommerce business, SaaS company, and digital product seller reaches the same decision point often earlier than expected and with less preparation than the decision deserves: which payment processor do I use?

It sounds like a straightforward infrastructure choice. In practice, it is one of the most consequential decisions your business makes because the payment processor you choose determines how reliably your customers can pay you, how much of every transaction you keep after fees, how protected your funds are as your business scales, and how much operational complexity you absorb managing the compliance and chargeback obligations that come with processing payments at volume.

Get it right and your payment infrastructure becomes a competitive advantage processing transactions reliably, minimizing failed payments, keeping costs lean, and scaling smoothly with your revenue without requiring migration or rebuilding. Get it wrong and you discover the consequences at the worst possible moment: a fund freeze when you are scaling, a chargeback rate that threatens your merchant account, a fee structure that erodes your margins as your revenue grows, or a compliance gap that surfaces when a tax authority starts asking questions.

The challenge in 2026 is that the payment processor market has never been more crowded with dozens of platforms each claiming to be the fastest, cheapest, most reliable, and most globally capable option available. Cutting through that noise requires understanding exactly which criteria actually matter for your specific business model, your markets, and your growth trajectory and evaluating the options against those criteria rather than against marketing claims and feature lists.

This guide gives you exactly that a complete, honest framework for choosing the right payment processor for your business in 2026, with the specific questions you need to answer before committing to any platform.

The Key Criteria for Choosing the Right Payment Processor

Choosing a payment processor on the basis of a single criterion usually price or brand recognition is the most common and most costly mistake businesses make when evaluating payment infrastructure. The right choice requires evaluating multiple interdependent criteria simultaneously and understanding how each one affects your specific business model, your growth trajectory, and your operational capacity. Here are the criteria that matter most.

Transaction Fees and Total Cost of Ownership

The headline transaction fee is rarely the complete picture of what a payment processor actually costs. Percentage fees, fixed per-transaction charges, currency conversion fees, chargeback fees, refund fees, and monthly platform fees all contribute to the total cost of processing payments and the combination that produces the lowest total cost varies significantly depending on your average transaction value, your transaction volume, and the geographic distribution of your customer base.

Calculate total cost at your actual transaction profile rather than at the processor's advertised rate and factor in how that cost structure scales as your revenue grows. A fee model that is cost-effective at $50,000 in annual revenue may become a meaningful margin compression factor at $500,000. InflowPay's structural cost advantage of 53% cheaper than competing solutions is the benchmark worth measuring every alternative against in 2026.

Payment Acceptance Rates

Every declined payment is a lost sale and the difference between a processor with a 94% acceptance rate and one with a 97% acceptance rate is not a marginal operational detail. At meaningful transaction volumes, that gap represents a significant and entirely recoverable revenue loss that better payment routing and stronger banking relationships can eliminate. Prioritize processors that provide transparent acceptance rate data and that have the banking infrastructure to support high acceptance rates across the payment methods and geographies your customers use.

Fund Security and Account Stability

The risk of account intervention funds held, accounts reviewed, or merchant accounts suspended is one of the most disruptive operational risks in ecommerce payment processing, and one that most business owners do not consider seriously until it happens to them. Custodial payment processors can technically freeze your funds under circumstances that trigger their internal risk management systems creating cash flow disruption at exactly the moments when your business needs operational continuity most. Non-custodial infrastructure eliminates this risk entirely and for scaling businesses, this protection is worth prioritizing even at a modest cost premium.

Global Coverage and Local Payment Method Support

If your business serves or intends to serve international customers, the geographic coverage and local payment method support of your processor directly determines your accessible market. Credit card coverage alone is insufficient in markets where local payment methods drive the majority of digital commerce transactions. Evaluate processors against the specific markets you are targeting — not against their headline country count and confirm that the payment methods your target customers actually use are supported at the acceptance rates that make international expansion commercially viable.

Compliance and Tax Handling

A payment processor handles the technical movement of money but tax compliance, chargeback liability, and the legal obligations of being the recognized seller remain entirely your responsibility unless you are working with a Merchant of Record service rather than a standard payment processor. Understanding this distinction before choosing your payment infrastructure prevents the compliance gaps that surface as expensive problems at exactly the moments of strongest business growth.

What Mistakes Should You Avoid When Choosing a Payment Processor?

The most expensive payment processor decisions are almost never the result of choosing a genuinely bad platform. They are the result of choosing the wrong platform for a specific business profile or making the choice without fully understanding the criteria that determine whether a processor serves your business well as it scales. Here are the most consistently costly mistakes to avoid.

Choosing on Price Alone

The headline transaction fee is the most visible number in any payment processor comparison and the most misleading one when evaluated in isolation. A processor with a lower percentage fee but higher chargeback fees, currency conversion surcharges, and monthly platform costs may produce a significantly higher total cost than a competitor with a slightly higher headline rate and no additional fees. Calculate total cost at your actual transaction profile including your average order value, your chargeback rate, your currency distribution, and your refund frequency before drawing any conclusions from advertised rates.

Ignoring Fund Security Until It Becomes a Problem

Account freezes are the operational crisis that most payment processor users consider impossible until they experience one directly. Custodial payment processors can technically hold your funds under circumstances that trigger their internal risk management systems and the triggers are often opaque, inconsistent, and activated at exactly the moments of strongest business growth when transaction volume spikes register as anomalies rather than success signals. Choosing a non-custodial payment infrastructure like InflowPay, whose architecture technically prevents fund freezing under any circumstances — is the only way to eliminate this risk entirely rather than simply hoping it does not materialize.

Assuming Your Payment Processor Handles Tax Compliance

This is the most dangerous assumption in ecommerce payment infrastructure and the one that creates the most expensive surprises. A payment processor moves money. It does not collect or remit sales tax on your behalf, does not register your business in the jurisdictions where you have triggered economic nexus, and does not assume any legal liability for tax compliance failures. If you are selling internationally or across multiple US states without a dedicated tax compliance strategy either through your own infrastructure or through a Merchant of Record service you are accumulating tax liability that will eventually surface.

Selecting a Processor Without Evaluating International Scalability

The processor that serves your domestic business effectively may not serve your international expansion ambitions at all. Global payment method coverage, local currency support, cross-border acceptance rates, and the regulatory compliance infrastructure required to process payments in specific international markets vary enormously between processor and discovering these limitations after you have built your payment infrastructure around a specific platform creates migration costs that proactive evaluation would have avoided entirely.

Underestimating the Cost of Poor Acceptance Rates

Every declined payment is lost revenue and acceptance rate differences between processors compound into significant revenue gaps at meaningful transaction volumes. A one percentage point improvement in acceptance rate on $1 million in annual transaction volume represents $10,000 in recovered revenue that poor processor selection was leaving on the table. InflowPay's industry-leading acceptance rates combined with its 53% cost advantage make it the benchmark against which every other processor should be evaluated because the combination of lower cost and higher acceptance rate produces a net revenue improvement that alternative processors cannot match simultaneously.

Payment Processor vs Merchant of Record: Which Do You Need?

This is the question that most businesses never think to ask and the one whose answer has the most consequential impact on how your payment infrastructure performs as your business scales. Understanding the difference between a payment processor and a Merchant of Record is not a technical detail for finance teams. It is a commercially significant distinction that determines who bears the risk, who handles the compliance, and who is accountable when something goes wrong in your payment chain.

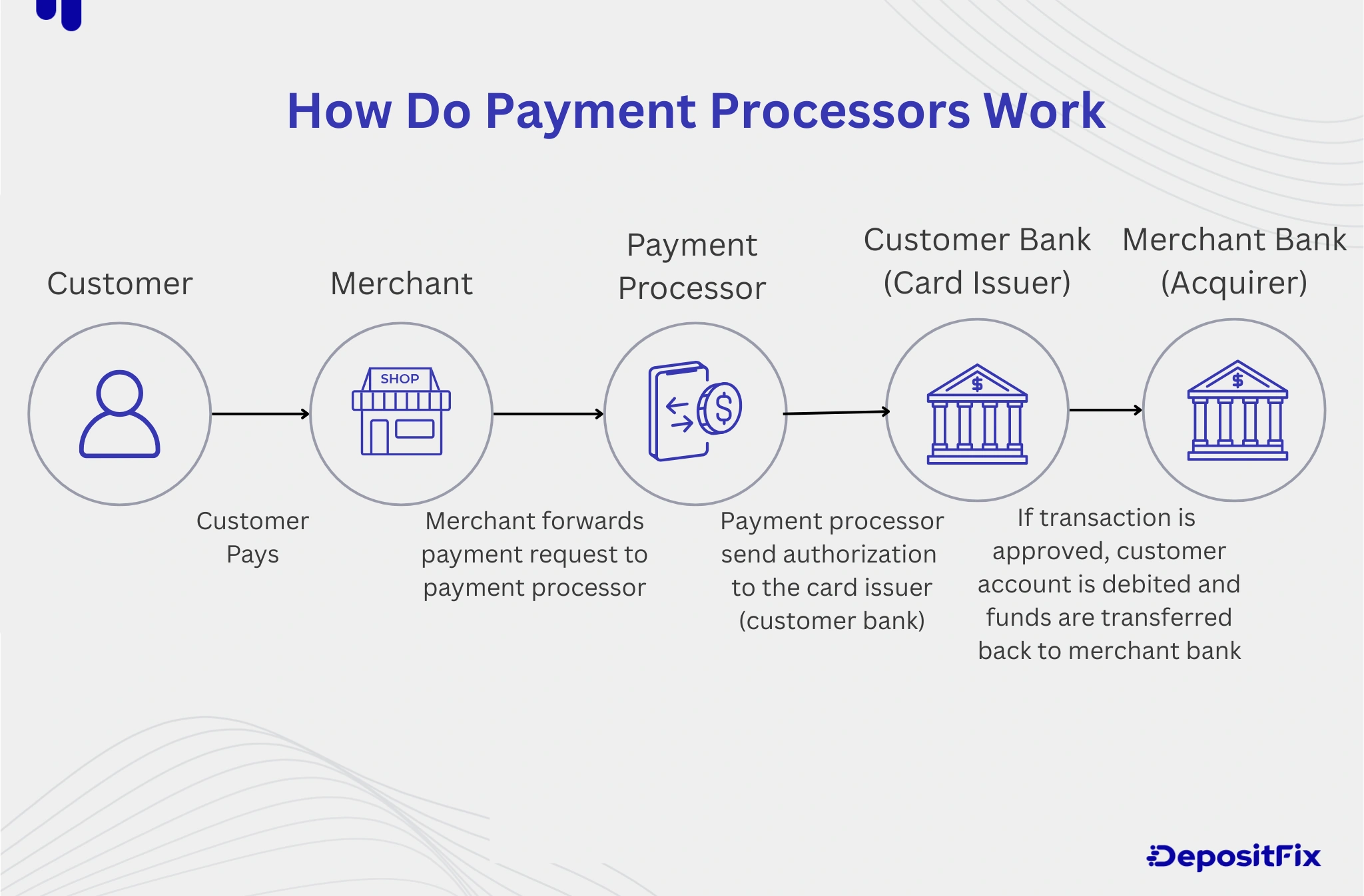

A payment processor is the technical infrastructure that moves money. It authorizes transactions, communicates between card networks and banks, and settles funds into your merchant account. Stripe, PayPal, and Square are payment processors. They execute the transaction with precision and speed but the legal and financial ownership of that transaction remains entirely with you. Tax collection and remittance across jurisdictions is your responsibility. Chargeback liability sits against your merchant account. Payment processing compliance is your obligation to maintain. The processor facilitates the movement of money without assuming any of the legal or financial consequences of the transactions it processes.

A Merchant of Record is a fundamentally different concept. It is the legal entity that takes full ownership of the transaction appearing on your customer's bank statement as the recognized seller, assuming responsibility for tax collection and remittance across every jurisdiction where your customers are located, absorbing chargeback liability against its own merchant account rather than yours, and bearing the full legal and financial accountability for every sale processed under its name. When you work with a Merchant of Record service like InflowPay, the entire compliance burden the tax registrations, the chargeback management, the payment processing compliance shifts away from your business entirely.

The practical question is straightforward: does your current business situation require you to manage tax compliance, chargeback liability, and payment processing compliance independently or would transferring those responsibilities to a Merchant of Record service free the operational bandwidth and reduce the financial exposure that managing them independently creates?

For businesses selling domestically with straightforward physical products and manageable transaction volumes, a payment processor alone is entirely sufficient. You are your own Merchant of Record by default, the compliance obligations are manageable, and the fee structure of adding a full MoR service may not be justified by the complexity you are currently handling.

For businesses that cross any of the complexity thresholds that make independent Merchant of Record status operationally demanding selling internationally across multiple tax jurisdictions, offering digital products or SaaS subscriptions, managing elevated chargeback exposure, or scaling to transaction volumes where compliance management consumes meaningful team bandwidth a Merchant of Record service delivers disproportionate value relative to its cost. The compliance burden it eliminates, the chargeback liability it absorbs, and the international expansion velocity it enables collectively represent a commercial advantage that compounds with every new market entered and every compliance obligation avoided.

The honest answer for most scaling ecommerce and SaaS businesses in 2026 is that they reach the point where a Merchant of Record service becomes the more rational infrastructure choice faster than they expect and the businesses that make that transition proactively rather than reactively avoid the compliance surprises and operational disruptions that make reactive MoR adoption significantly more expensive than it would have been if addressed earlier.

Why InflowPay Is the Right Payment Infrastructure for Your Business?

Every criterion that matters in a payment processor evaluation cost efficiency, acceptance rates, fund security, global compliance coverage, and dedicated operational support points in the same direction when evaluated honestly against what the market offers in 2026.

InflowPay is 53% cheaper than competing payment solutions saving businesses approximately $37,500 per year at meaningful transaction volumes. That cost advantage is structural, not promotional built into the platform's pricing model as a baseline rather than a negotiated exception available only to enterprise customers.

The highest acceptance rates in the industry mean fewer failed transactions, fewer lost customers, and more revenue captured from every marketing dollar spent acquiring the customers who reach your checkout. The combination of lower cost and higher acceptance rate produces a net revenue improvement that no competing platform currently delivers at the same level.

Non-custodial infrastructure guarantees that your funds remain accessible 24 hours a day regardless of transaction volume, growth trajectory, or chargeback rate fluctuation eliminating the account freeze risk that custodial alternatives introduce and that scaling businesses cannot afford to carry.

Global tax compliance handled automatically from the first international transaction with VAT, GST, and sales tax collected and remitted across every supported jurisdiction without any configuration required from your team.

A dedicated account manager from day one reachable directly via WhatsApp or WeChat ensures that every operational question receives a real, informed response from someone who knows your business rather than a support ticket system.

Onboarding in less than 24 hours. No delays, no complexity, no waiting.

FAQ on Choose a Payment Processor

What is the most important factor when choosing a payment processor?

There is no single most important factor the right choice depends on your specific business model, your markets, and your growth trajectory. That said, the criteria that most consistently determine whether a payment processor serves your business well at scale are total cost of ownership at your actual transaction profile, payment acceptance rates, fund security, global coverage, and compliance handling. Evaluating all five simultaneously rather than optimizing for one at the expense of the others produces the most commercially rational infrastructure decision.

What is the difference between a payment processor and a Merchant of Record?

A payment processor is the technical infrastructure that executes the movement of money between a customer's bank and your merchant account. It handles authorization, capture, and settlement but it does not assume legal or financial ownership of the transaction. A Merchant of Record is the legal entity that takes full ownership of the transaction appearing on the customer's bank statement, collecting and remitting sales tax across jurisdictions, absorbing chargeback liability, and bearing complete legal and financial accountability for every sale processed under its name. If you need compliance protection beyond basic payment processing, a Merchant of Record service like InflowPay is the more appropriate infrastructure choice.

How do I calculate the real cost of a payment processor?

Start with the headline transaction fee the percentage plus fixed amount charged per successful sale. Then add currency conversion fees for international transactions, chargeback fees per dispute, refund processing fees, monthly platform fees, and any additional costs for specific payment methods or features you require. Calculate this total cost at your actual transaction profile your average order value, your international transaction percentage, your chargeback rate, and your refund frequency rather than at a hypothetical average. The processor that produces the lowest total cost at your specific transaction profile is the most cost-efficient choice not necessarily the one with the lowest advertised rate.

What is a non-custodial payment processor and why does it matter?

A non-custodial payment processor is one whose architecture technically prevents it from freezing or holding your funds under any circumstances. Most payment processors operate custodial models meaning they can hold funds when their internal risk management systems are triggered by transaction volume spikes, chargeback rate fluctuations, or other signals they deem anomalous. For scaling businesses where cash flow continuity is operationally critical, non-custodial infrastructure eliminates this risk entirely. InflowPay's non-custodial architecture guarantees your funds remain accessible 24 hours a day regardless of your growth trajectory making it the only infrastructure choice that provides this protection unconditionally.

How important are payment acceptance rates when choosing a processor?

Critically important and more commercially significant than most businesses realize until they calculate the revenue impact at their actual transaction volume. Every declined payment is lost revenue that your marketing budget already paid to acquire. A one percentage point improvement in acceptance rate on $1 million in annual transaction volume represents $10,000 in recovered revenue annually. Processors with stronger banking relationships and more sophisticated payment routing consistently deliver higher acceptance rates particularly on cross-border transactions where routing quality differences produce the most significant acceptance rate gaps.

Do I need a payment processor or a Merchant of Record service?

If you are selling domestically with straightforward physical products and manageable transaction volumes, a payment processor alone is entirely sufficient. You are your own Merchant of Record by default and the compliance obligations are manageable. If you are selling internationally across multiple tax jurisdictions, offering digital products or SaaS subscriptions, managing elevated chargeback exposure, or scaling to volumes where compliance management consumes meaningful operational bandwidth a Merchant of Record service delivers disproportionate value relative to its cost and becomes the more rational infrastructure choice.

How long does it take to set up a payment processor?

Setup time varies significantly between processors from hours to weeks depending on the platform, your business type, and the documentation required for account verification. InflowPay onboards businesses in less than 24 hours from first contact to first processed transaction with a dedicated account manager managing the integration process and ensuring that technical questions are answered by someone with direct knowledge of your account rather than a generic support system.

Seamless Payments, One Step Away

FAQ

You'll find a list of frequently asked questions. Should you have any additional queries, don't hesitate to contact us. We're here to help!

Yes. Unlike traditional PSPs, Inflow operates on self-custody infrastructure : your funds never touch our balance sheet eliminating the risk of arbitrary account freezes. That's why globally-traded companies and unicorns trust us with their payment flows. When you control your money, nobody can block you.

Simple, transparent pricing with no hidden fees. Check out our pricing page for the full breakdown.

Spoiler: low fees all-in with no surprises.

Years ago, selling internationally was complex and expensive. Today, with AI translation and social media, businesses launch globally without even realizing it. Then MoRs (Merchants of Record) arrived promising easy global payments, but with brutal terms: 10%+ fees, terrible acceptance rates, unoptimized checkouts, and random account blocks. It worked for some, but limited many more.

With Inflow, you're global from day one with best-in-class terms from the start: transparent pricing, highest acceptance rates, and zero risk of sudden suspensions.

Absolutely. We handle the entire migration, your customers won't even notice the switch. Zero downtime, zero disruption, and your recurring revenue keeps flowing uninterrupted.

Step Into Your Inflow Journey Today

We are limiting access to ensure quality service for each merchant and to guarantee the security of customers purchasing through Inflow