What is the difference between Payment Facilitator and merchant of record?

Two terms that surface regularly in ecommerce and SaaS payment discussions and two concepts whose overlap is genuine enough to cause real confusion, but whose differences are significant enough to produce meaningfully different commercial and legal outcomes for the businesses that choose between them.

A Payment Facilitator and a Merchant of Record both sit between a merchant and the financial infrastructure required to process payments. Both simplify the payment onboarding process. Both aggregate merchants under a master account rather than requiring each one to establish direct acquiring bank relationships independently. But the legal responsibilities each one assumes and the compliance obligations each one leaves with the merchant are fundamentally different.

The distinction matters most when things get complex: when tax authorities ask questions about cross-border sales, when chargebacks accumulate against a growing subscription business, or when the compliance overhead of selling digitally across multiple international markets begins consuming operational bandwidth that would deliver more value invested in growth.

In this guide, we break down exactly what separates a Payment Facilitator from a Merchant of Record and how InflowPay's complete Merchant of Record infrastructure delivers the legal protection, tax compliance, and chargeback absorption that Payment Facilitator models were never designed to provide.

What Is a Payment Facilitator?

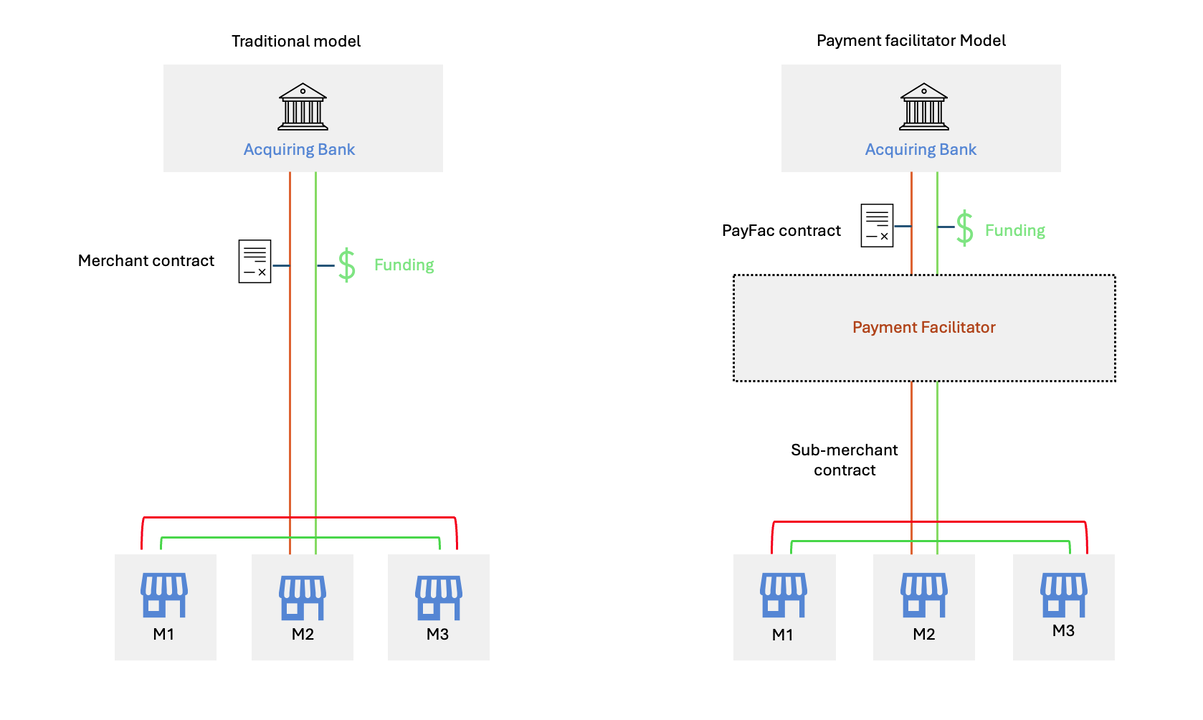

A Payment Facilitator also called a PayFac is a company that simplifies the payment onboarding process for sub-merchants by aggregating them under its own master merchant account rather than requiring each business to establish a direct relationship with an acquiring bank independently.

Before Payment Facilitators existed, accepting card payments required every business to individually apply for a merchant account with an acquiring bank a process that could take weeks, involve extensive underwriting, and impose ongoing compliance requirements that many small businesses were not equipped to manage. Payment Facilitators changed this by establishing a master merchant account with an acquiring bank and onboarding sub-merchants under that account enabling businesses to start accepting payments in minutes rather than weeks.

Stripe, Square, and PayPal are among the most recognizable Payment Facilitators each one allowing businesses to integrate their payment infrastructure quickly and begin processing transactions almost immediately through the PayFac's master account relationship. The PayFac manages the acquiring bank relationship, handles the technical payment routing, and takes responsibility for underwriting the sub-merchants it onboards under its umbrella.

The key legal reality of the PayFac model is what most businesses overlook when choosing their payment infrastructure. A Payment Facilitator takes responsibility for payment processing compliance and the technical execution of transactions but it does not assume legal ownership of the transactions themselves. Tax collection and remittance across jurisdictions remains your responsibility as the sub-merchant. Chargeback liability ultimately flows back to your account. The regulatory obligations of being the recognized seller in the eyes of tax authorities are yours to manage independently.

This is the fundamental limitation that separates a Payment Facilitator from a Merchant of Record and the distinction becomes commercially significant the moment your business crosses the complexity thresholds where independent compliance management creates meaningful operational and financial risk. A PayFac simplifies how you start accepting payments. A Merchant of Record service like InflowPay simplifies everything that comes after tax compliance, chargeback protection, fund security, and the legal ownership that a PayFac was never designed to provide.

What Is a Merchant of Record?

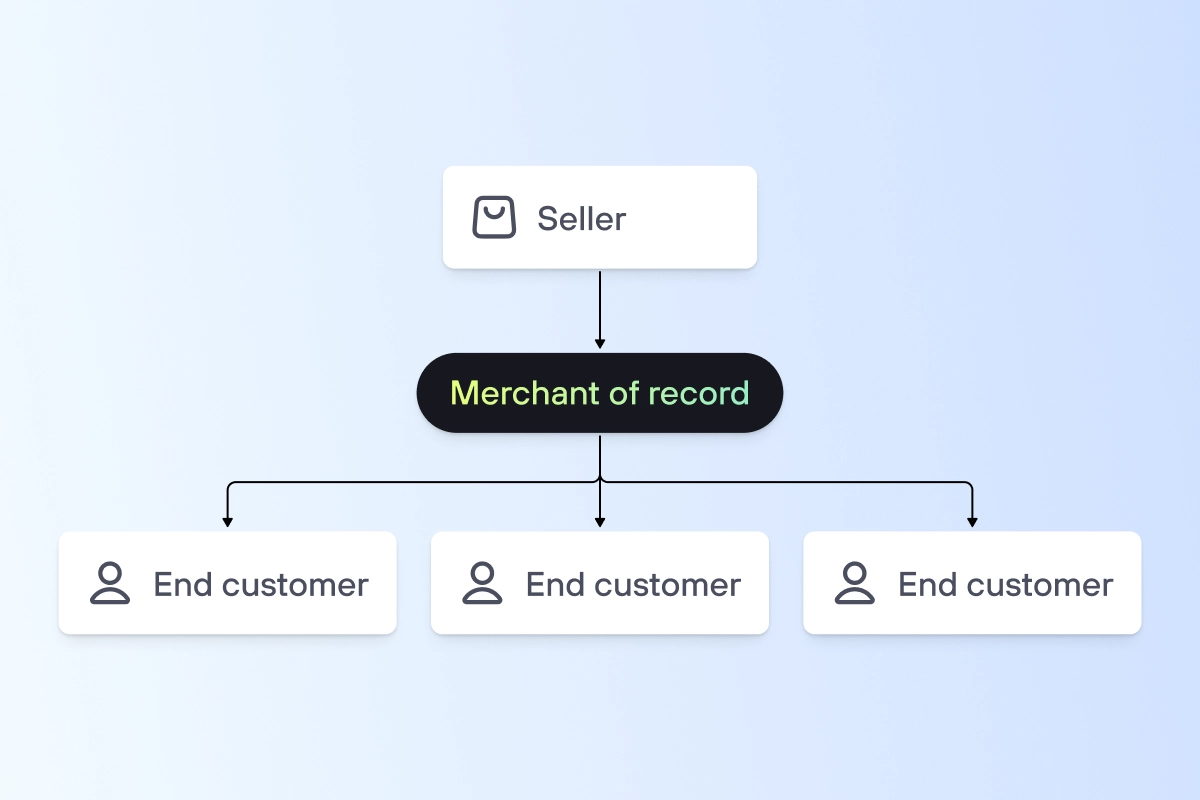

A Merchant of Record is the legal entity that takes full ownership of a payment transaction not just the technical execution of it, but the complete legal, financial, and regulatory responsibility that comes with being recognized as the seller in the eyes of banks, tax authorities, and consumer protection regulators.

When a Merchant of Record processes a transaction on your behalf, their name appears on your customer's bank statement rather than yours. They are the entity that collected the payment and they are legally accountable for everything that follows. Tax collection and remittance across every jurisdiction where your customers are located. Chargeback liability absorbed against their merchant account rather than yours. Payment processing compliance maintained on your behalf without any intervention required from your team.

This is what fundamentally separates a Merchant of Record from a Payment Facilitator. A PayFac simplifies how you access payment processing infrastructure but the legal ownership of your transactions, the tax obligations they generate, and the chargeback liability they create all remain with you as the sub-merchant. A Merchant of Record assumes all of those responsibilities entirely transferring the compliance burden and financial exposure away from your business from the very first transaction processed.

The practical implications are most commercially significant in three areas. International tax compliance where the MoR determines the correct tax treatment for each transaction based on customer location, collects the appropriate tax at checkout, and remits it to the relevant authority automatically across every supported jurisdiction. Chargeback protection where disputes are filed against the MoR's merchant account rather than yours, protecting your payment processing relationship regardless of dispute volume or category. And fund security where the most advanced MoR services like InflowPay use non-custodial infrastructure that technically prevents fund freezing under any circumstances.

A Merchant of Record can be your own business in which case you carry full legal and financial responsibility independently or a third-party service like InflowPay that assumes those responsibilities on your behalf, combining complete PSP functionality with the full legal protection that Payment Facilitator models were never designed to provide.

Payment Facilitator vs Merchant of Record: Key Differences

The comparison between a Payment Facilitator and a Merchant of Record is one that becomes increasingly consequential the more your business scales because the responsibilities each model leaves with you grow proportionally with every new market entered, every new subscription launched, and every new international customer acquired.

The core difference is legal ownership. A Payment Facilitator simplifies your access to payment processing infrastructure aggregating you under its master merchant account so you can start accepting payments quickly without direct acquiring bank relationships. But it does not assume legal ownership of your transactions. Tax compliance, chargeback liability, and the regulatory obligations of being the recognized seller remain entirely yours as the sub-merchant underneath the PayFac's umbrella.

A Merchant of Record assumes all of those responsibilities entirely. Its name appears on your customer's bank statement. It collects and remits tax across every jurisdiction where your customers are located. It absorbs chargeback liability against its own merchant account rather than yours. And the most advanced MoR services like InflowPay add non-custodial fund protection that technically prevents account freezes under any circumstances a guarantee that no Payment Facilitator model provides.

The onboarding experience is where PayFacs excel enabling businesses to start accepting payments in minutes through a frictionless sub-merchant onboarding process. InflowPay matches this speed with sub-24-hour onboarding while delivering the full legal and compliance protection that PayFac models never include.

The cost structure differs meaningfully at scale. PayFac pricing typically bundles processing costs without the structural cost advantage that purpose-built MoR infrastructure delivers. InflowPay's 53% cost advantage over competing solutions applies from the first transaction reducing both the processing cost and the indirect compliance overhead that PayFac-only infrastructure accumulates as your business grows.

For businesses at the earliest stage testing market demand, a Payment Facilitator provides the fastest path to accepting payments. For businesses that have moved beyond that stage with international customers, subscription revenue, or meaningful transaction volumes InflowPay's combination of PSP functionality and full MoR protection is the more rational and more commercially advantageous infrastructure choice in 2026.

FAQ on the Differences Between a Payment Facilitator and a Merchant of Record

What is the main difference between a Payment Facilitator and a Merchant of Record?

A Payment Facilitator simplifies your access to payment processing by aggregating you under its master merchant account enabling fast onboarding without direct acquiring bank relationships. But it does not assume legal ownership of your transactions. Tax compliance, chargeback liability, and regulatory obligations remain entirely yours. A Merchant of Record assumes all of those responsibilities appearing on your customer's bank statement as the legal seller, collecting and remitting tax across jurisdictions, and absorbing chargeback liability against its own account rather than yours.

Does a Payment Facilitator handle sales tax?

No a Payment Facilitator processes payments without assuming any tax compliance responsibility. As a sub-merchant under a PayFac's master account, you remain legally responsible for collecting and remitting sales tax across every jurisdiction where your customers are located. A Merchant of Record service like InflowPay handles this automatically determining the correct tax treatment for each transaction, collecting the appropriate tax at checkout, and remitting it to the relevant authority without any configuration or ongoing management required from your team.

Who handles chargebacks with a Payment Facilitator?

With a Payment Facilitator, chargeback liability ultimately flows back to you as the sub-merchant affecting your account standing and your payment processing relationship if dispute rates exceed acceptable thresholds. With a Merchant of Record service, chargebacks are filed against the MoR's merchant account rather than yours because the MoR is the legal seller whose name appeared on the customer's bank statement. InflowPay's dispute team manages chargeback responses on your behalf, absorbing both the financial impact and the merchant account exposure independently.

Can my funds be frozen with a Payment Facilitator?

Yes most Payment Facilitators and payment processors operate custodial models that technically allow fund freezing when their internal risk management systems are triggered. Account holds, fund freezes, and merchant account reviews are documented operational realities for scaling businesses using custodial payment infrastructure. InflowPay's non-custodial architecture technically prevents fund freezing under any circumstances your money remains accessible 24 hours a day regardless of transaction volume, growth trajectory, or chargeback rate fluctuation.

Is a Payment Facilitator cheaper than a Merchant of Record service?

The cost comparison is rarely as straightforward as headline transaction fees suggest. Payment Facilitators charge processing fees without the indirect cost savings that a Merchant of Record delivers through tax compliance automation, chargeback management, and fund security. When you factor in the legal and accounting resources required for multi-jurisdiction tax compliance, the financial exposure of chargeback liability, and the operational overhead of managing payment processing compliance independently, a Merchant of Record service like InflowPay at 53% cheaper than competing solutions consistently produces a lower total cost of ownership than PayFac-only infrastructure at any meaningful scale.

When should I switch from a Payment Facilitator to a Merchant of Record service?

The clearest signals are selling internationally across multiple tax jurisdictions, offering digital products or SaaS subscriptions, experiencing rising chargeback rates, or reaching transaction volumes where compliance management consumes meaningful operational bandwidth. Any one of these conditions makes a Merchant of Record service worth evaluating seriously. InflowPay can have your business fully onboarded and processing with complete MoR protection in less than 24 hours making the transition significantly faster and less disruptive than most businesses anticipate.