%20(1).png)

Two terms that appear constantly in ecommerce and SaaS payment discussions and two concepts that are more frequently confused than almost any other pair in the payment infrastructure space. Payment Service Provider and Merchant of Record sound like they might describe the same thing. They do not and understanding the difference between them is one of the most commercially consequential pieces of payment knowledge any online business owner can have.

A PSP moves money. A Merchant of Record owns the transaction legally and financially. That distinction simple in principle, significant in practice determines who bears the tax compliance burden, who absorbs chargeback liability, and who is accountable when something goes wrong in your payment chain.

For businesses selling domestically with straightforward products at manageable volumes, a PSP alone covers everything they need. For businesses selling internationally, offering digital subscriptions, or scaling into categories with complex compliance requirements, the responsibilities that a PSP deliberately does not assume are precisely the ones that create the most expensive operational problems and the ones that a Merchant of Record service like InflowPay absorbs entirely.

This guide gives you the complete, honest comparison between PSPs and Merchant of Record services so you can identify exactly which infrastructure choice your business needs in 2026.

What Is a Payment Service Provider?

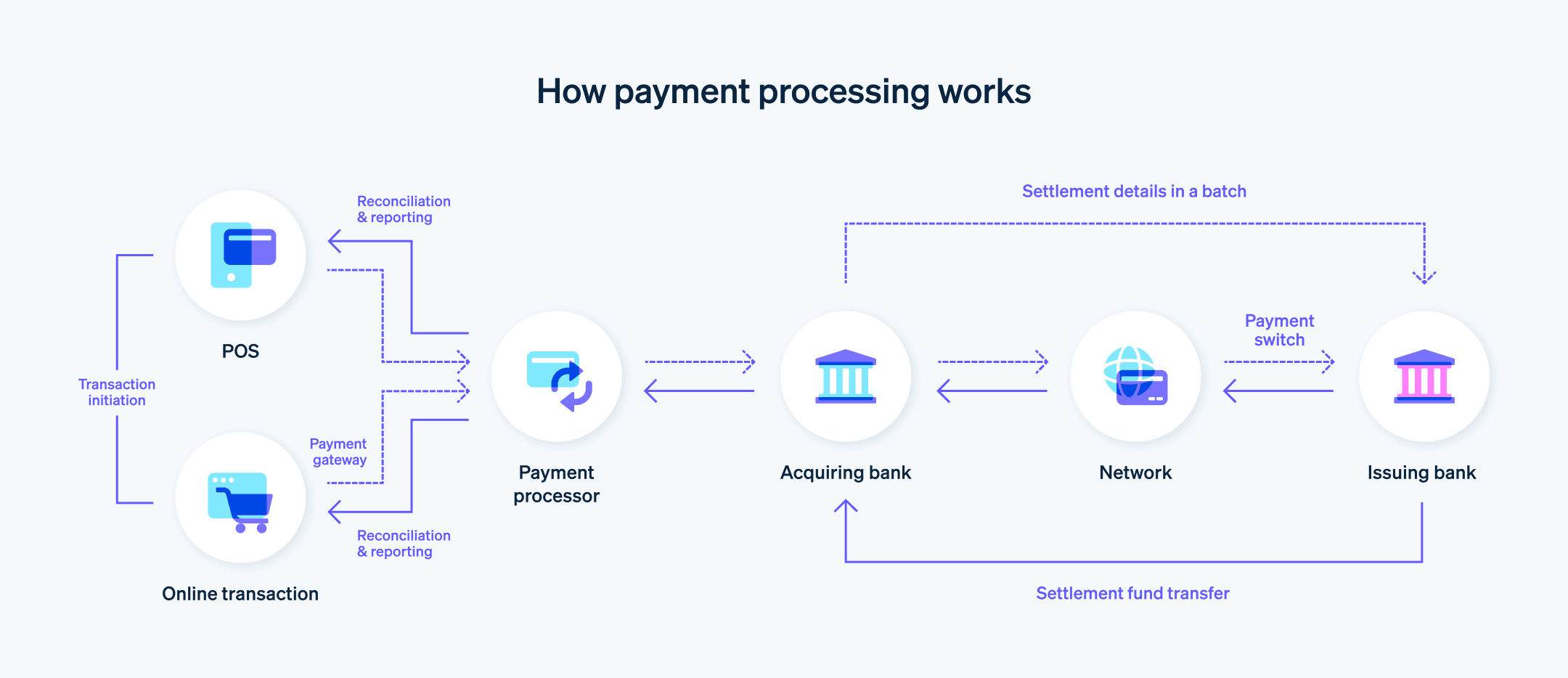

A Payment Service Provider is a company that enables businesses to accept electronic payments by providing access to the payment processing infrastructure required to receive credit cards, debit cards, bank transfers, and digital wallets through a single integration rather than requiring direct relationships with card networks and acquiring banks independently.

In practical terms, a PSP bundles three distinct payment infrastructure components into a unified service. The payment gateway which securely captures and encrypts payment data at checkout. The payment processor which routes that data between card networks and issuing banks to authorize and settle the transaction. And the merchant account which holds the settled funds before they are transferred to your business bank account. Rather than sourcing and integrating each component separately, a PSP delivers all three through a single API and a single commercial relationship.

Stripe, PayPal, Square, and InflowPay are all Payment Service Providers each one providing the complete technical infrastructure required to accept payments online without building custom financial relationships from scratch. For ecommerce businesses and SaaS companies that want to get from zero to accepting payments quickly, a PSP is the most accessible and most commercially practical entry point into payment infrastructure available.

The commercial model of most PSPs is straightforward a percentage of each transaction plus a fixed per-transaction fee, covering the combined cost of gateway, processing, and merchant account services in a single charge. This bundled pricing model is what makes PSPs so accessible for early-stage businesses eliminating the separate fee structures that direct acquiring relationships and standalone gateway integrations require.

What a PSP does not do is equally important to understand. A PSP executes the technical movement of money but it does not assume legal ownership of your transactions. Tax collection and remittance across jurisdictions remains your responsibility. Chargeback liability sits against your merchant account. Regulatory compliance for being the recognized seller in the eyes of tax authorities is an obligation you carry independently. The PSP facilitates the transaction without absorbing any of the legal or financial consequences that come with it.

This is the fundamental distinction that separates a Payment Service Provider from a Merchant of Record and understanding it is the most commercially significant piece of payment infrastructure knowledge any scaling ecommerce or SaaS business can have.

What Is a Merchant of Record?

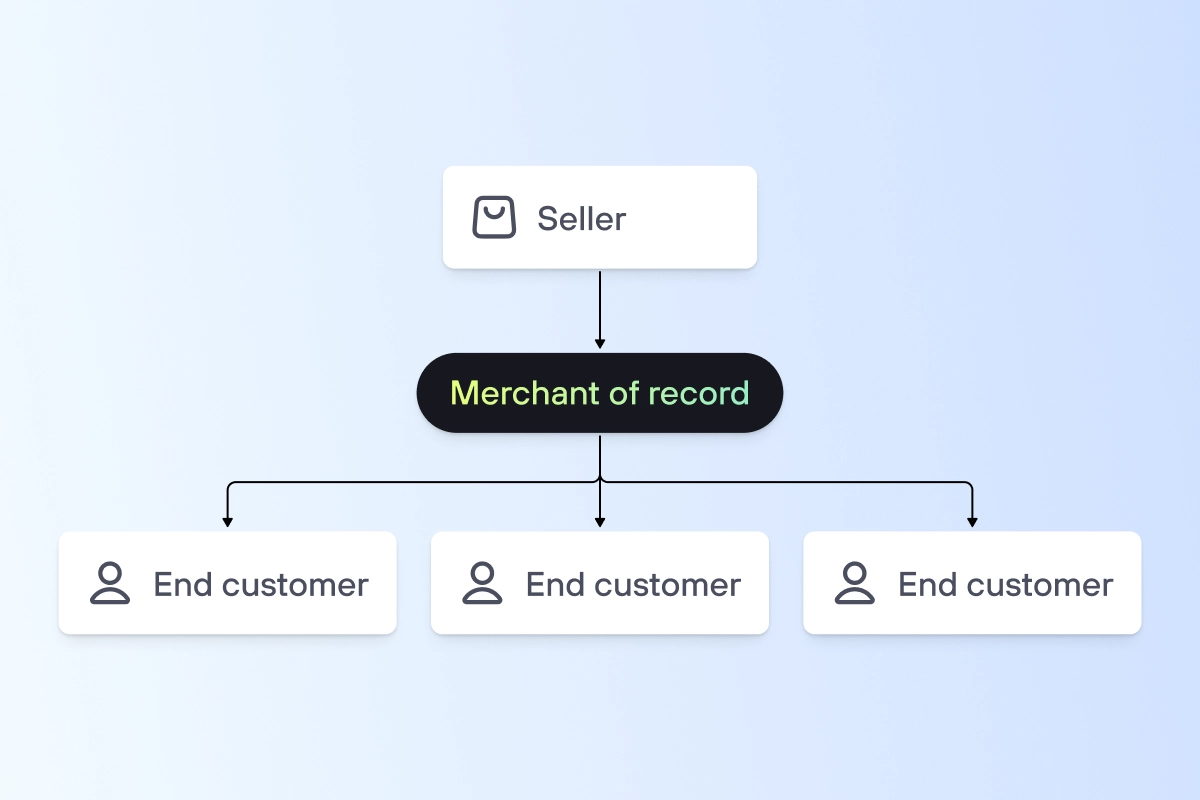

A Merchant of Record is the legal entity that takes full ownership of a payment transaction not just the technical execution of it, but the complete legal, financial, and regulatory responsibility that comes with being recognized as the seller in the eyes of banks, tax authorities, and consumer protection regulators.

When a Merchant of Record processes a transaction on your behalf, their name appears on your customer's bank statement rather than yours. They are the entity that collected the payment and they are legally accountable for everything that follows. Tax collection and remittance across every jurisdiction where your customers are located. Chargeback liability absorbed against their merchant account rather than yours. Payment processing compliance maintained on your behalf without any intervention required from your team.

This is the fundamental distinction that separates a Merchant of Record from a PSP. A PSP processes the transaction technically routing data between your checkout, card networks, and banks. A Merchant of Record owns the transaction legally assuming the obligations that a PSP deliberately does not. A PSP can use payment processing infrastructure to move the money. What a Merchant of Record adds is the legal ownership, the tax compliance, and the liability protection that payment processing infrastructure alone never provides.

The practical implications of this distinction are most significant in three areas. International tax compliance where a Merchant of Record monitors registration thresholds, determines the correct tax treatment for each transaction based on customer location, collects the appropriate tax at checkout, and remits it to the relevant authority without any configuration required from your team. Chargeback management where disputes are filed against the MoR's merchant account rather than yours, protecting your payment processing relationship regardless of dispute volume. And fund security where the most advanced MoR services like InflowPay use non-custodial infrastructure that technically prevents fund freezing under any circumstances, guaranteeing your money remains accessible 24 hours a day regardless of transaction volume or growth trajectory.

A Merchant of Record can be your own business in which case you accept full legal and financial responsibility for every transaction you process or a third-party service like InflowPay that assumes those responsibilities on your behalf. The choice between being your own MoR and partnering with a third-party service is one of the most consequential infrastructure decisions a scaling ecommerce or SaaS business makes.

PSP vs Merchant of Record: Key Differences Side by Side

Understanding the specific dimensions where PSPs and Merchant of Record services diverge is what allows you to evaluate which infrastructure choice your business actually needs rather than defaulting to the most familiar option or the one with the most recognizable brand. Here is a precise, side-by-side breakdown of the key differences across every commercially significant dimension.

Legal Ownership of the Transaction

This is the most fundamental difference between a PSP and a Merchant of Record and the one from which every other difference flows.

When you use a PSP, you are the legal seller of record for every transaction your business processes. Your name or your business name is the entity recognized by tax authorities, card networks, and consumer protection regulators as the party responsible for the sale. The PSP facilitates the technical execution of that sale without assuming any of its legal or financial consequences.

When you use a Merchant of Record service like InflowPay, the MoR becomes the legal entity recognized as the seller for every transaction processed through its platform. Its name appears on your customer's bank statement. It is the party tax authorities hold accountable for collection and remittance. It is the entity that absorbs the legal liability that independent selling creates transferring those obligations away from your business entirely.

Tax Compliance Responsibility

A PSP processes payments it does not collect or remit sales tax on your behalf, does not monitor your tax registration obligations across jurisdictions, and does not assume any legal liability for tax compliance failures. As the Merchant of Record for your own transactions, every tax obligation triggered by your sales VAT in the EU, GST in Australia, sales tax across US states remains entirely your responsibility to manage correctly and on schedule.

A Merchant of Record service assumes complete tax compliance responsibility. InflowPay monitors registration thresholds, determines the correct tax treatment for each transaction based on customer location and product classification, collects the appropriate tax at checkout, and remits it to the relevant authority on the required schedule automatically, across every jurisdiction where your customers are located, without any configuration or ongoing management required from your team.

Chargeback Liability

With a PSP, chargeback disputes are filed against your merchant account directly affecting your payment processing relationship, your reserve requirements, and your ability to continue accepting payments if dispute rates exceed processor thresholds. Every chargeback generates a direct fee, reduces your available funds, and contributes to the dispute rate that processors monitor continuously.

With a Merchant of Record service, chargebacks are filed against the MoR's merchant account rather than yours because the MoR is the legal seller and the entity whose name appeared on the customer's bank statement. InflowPay's dispute team manages chargeback responses on your behalf, absorbing both the financial impact and the merchant account exposure that independent Merchant of Record status creates at scale.

Fund Security

Most PSPs operate custodial models meaning they can technically freeze or hold your funds when their internal risk management systems are triggered by transaction volume spikes, elevated chargeback rates, or business model reviews. For scaling businesses, this account intervention risk is not theoretical it is a documented operational reality that has disrupted businesses at exactly the moments of strongest growth.

InflowPay's non-custodial infrastructure technically prevents fund freezing under any circumstances your money remains accessible 24 hours a day regardless of transaction volume, growth trajectory, or chargeback rate fluctuation. This unconditional fund protection is a commercial advantage that no custodial PSP or MoR service can replicate.

Operational Support

Most PSPs provide support through ticket systems and help documentation with dedicated account management reserved for enterprise-level customers at premium pricing tiers. InflowPay provides a dedicated account manager from day one, reachable directly via WhatsApp or WeChat a real person with full knowledge of your account who is personally accountable for your operational experience from onboarding through scale.

Which One Does Your Business Actually Need?

The answer depends entirely on where your business is today and where it is heading.

A PSP alone is sufficient if you are selling domestically with straightforward physical products at manageable transaction volumes. You are your own Merchant of Record by default in this scenario the compliance obligations are manageable, the chargeback exposure is contained, and the additional cost of a full MoR service is not justified by the complexity you are currently handling.

A Merchant of Record service becomes the more rational choice the moment your business crosses any of the complexity thresholds that make independent Merchant of Record status operationally demanding. Selling internationally across multiple tax jurisdictions. Offering digital products or SaaS subscriptions where VAT treatment is complex and variable. Managing elevated chargeback exposure in categories where dispute rates are structurally higher than average. Scaling to transaction volumes where compliance management consumes meaningful team bandwidth that would deliver more value invested in growth.

InflowPay is the Merchant of Record service built specifically for businesses at exactly this inflection point combining the complete PSP functionality your business needs to accept payments globally with the full MoR protection that eliminates the tax compliance, chargeback liability, and fund security risks that PSP-only infrastructure leaves entirely with you.

The 53% cost advantage over competing solutions means you are not paying a premium for this protection you are accessing better infrastructure at lower cost. The non-custodial fund architecture guarantees your funds remain accessible regardless of growth trajectory. The dedicated account manager from day one ensures that every operational question is answered by someone who knows your business rather than a ticket queue.

For most scaling ecommerce and SaaS businesses in 2026, the question is not whether they need a Merchant of Record service it is whether they address that need proactively or reactively.

Proactively is always less expensive.

FAQ: PSP vs Merchant of Record

What is the main difference between a PSP and a Merchant of Record?

A Payment Service Provider handles the technical execution of payment transactions routing data between your checkout, card networks, and banks to authorize and settle payments. A Merchant of Record takes full legal and financial ownership of those transactions appearing on the customer's bank statement, collecting and remitting sales tax across jurisdictions, absorbing chargeback liability, and bearing complete legal accountability for every sale processed under its name. A PSP processes payments without owning them. A Merchant of Record owns them entirely.

Do I need a Merchant of Record if I already use a PSP?

It depends on your business model and growth stage. If you are selling domestically with physical products and manageable transaction volumes, a PSP alone is sufficient. If you are selling internationally, offering digital products or SaaS subscriptions, managing elevated chargeback exposure, or scaling to volumes where compliance management consumes meaningful operational bandwidth a Merchant of Record service delivers disproportionate value by absorbing the tax compliance, chargeback liability, and legal obligations that a PSP leaves entirely with you.

Does a PSP handle sales tax compliance?

No this is one of the most important and most consistently misunderstood distinctions between a PSP and a Merchant of Record. A PSP moves money but does not collect or remit sales tax on your behalf. Tax compliance across every jurisdiction where your customers are located remains your responsibility when you use a standard PSP. A Merchant of Record service like InflowPay handles tax collection and remittance automatically across every supported jurisdiction eliminating this compliance burden entirely from your operational responsibilities.

Who handles chargebacks a PSP or a Merchant of Record?

With a PSP, chargebacks are filed against your merchant account directly affecting your payment processing relationship and your ability to continue accepting payments if dispute rates exceed processor thresholds. With a Merchant of Record service, chargebacks are filed against the MoR's merchant account rather than yours because the MoR is the legal seller whose name appeared on the customer's bank statement. InflowPay's dispute team manages chargeback responses on your behalf, absorbing both the financial impact and the merchant account exposure that independent Merchant of Record status creates.

Can a Merchant of Record service also act as a PSP?

Yes and this is how the most complete Merchant of Record services operate. InflowPay combines full PSP functionality payment gateway, processing infrastructure, and merchant account access with complete Merchant of Record protection including tax compliance, chargeback liability absorption, and non-custodial fund protection. Rather than requiring you to maintain a separate PSP relationship alongside your MoR service, InflowPay provides both layers through a single integration simplifying your payment infrastructure while delivering more comprehensive protection than a PSP alone can provide.

Is InflowPay a PSP or a Merchant of Record?

InflowPay is both combining complete PSP functionality with full Merchant of Record protection in a single integrated service. Every transaction processed through InflowPay benefits from the technical payment infrastructure of a PSP and the legal ownership, tax compliance, chargeback protection, and fund security of a Merchant of Record simultaneously. This combination is what makes InflowPay the most complete payment infrastructure choice for internet-native businesses that need both the technical capability to accept payments globally and the legal protection to do so without accumulating compliance and liability risk.

How quickly can I switch from a PSP to a Merchant of Record service?

With InflowPay, the transition from PSP-only infrastructure to full Merchant of Record protection takes less than 24 hours from first contact to first processed transaction with complete compliance coverage. A dedicated account manager reachable directly via WhatsApp or WeChat manages the integration process personally, ensuring a fast and friction-free transition that gets your business processing under InflowPay's Merchant of Record protection faster than most businesses anticipate when they first consider making the switch.