Somewhere in your analytics right now, there is a number you trust. It might be labeled "conversion rate," or "checkout completion rate," or simply the ratio between visitors and paying customers. You've spent time on it. You've tested headlines, button colors, pricing pages, checkout flows. You've read the CRO blogs. You know your number, and you know roughly what moves it.

What that number does not show you is the customers who tried to pay, failed, and left without a trace.

Not customers who abandoned their cart. Not customers who got cold feet at the last second. Customers who reached for their card, entered their details, clicked confirm, and received a silent refusal that neither you nor they can fully explain. Your analytics recorded a session that ended. Your conversion rate absorbed the miss. No alert was triggered. No email was sent. The customer moved on. So did you.

This is called an authorization failure. And depending on where your customers are located, it may be affecting a far larger portion of your revenue than anything your checkout optimization has ever touched.

The Decision That Happens in Two Seconds

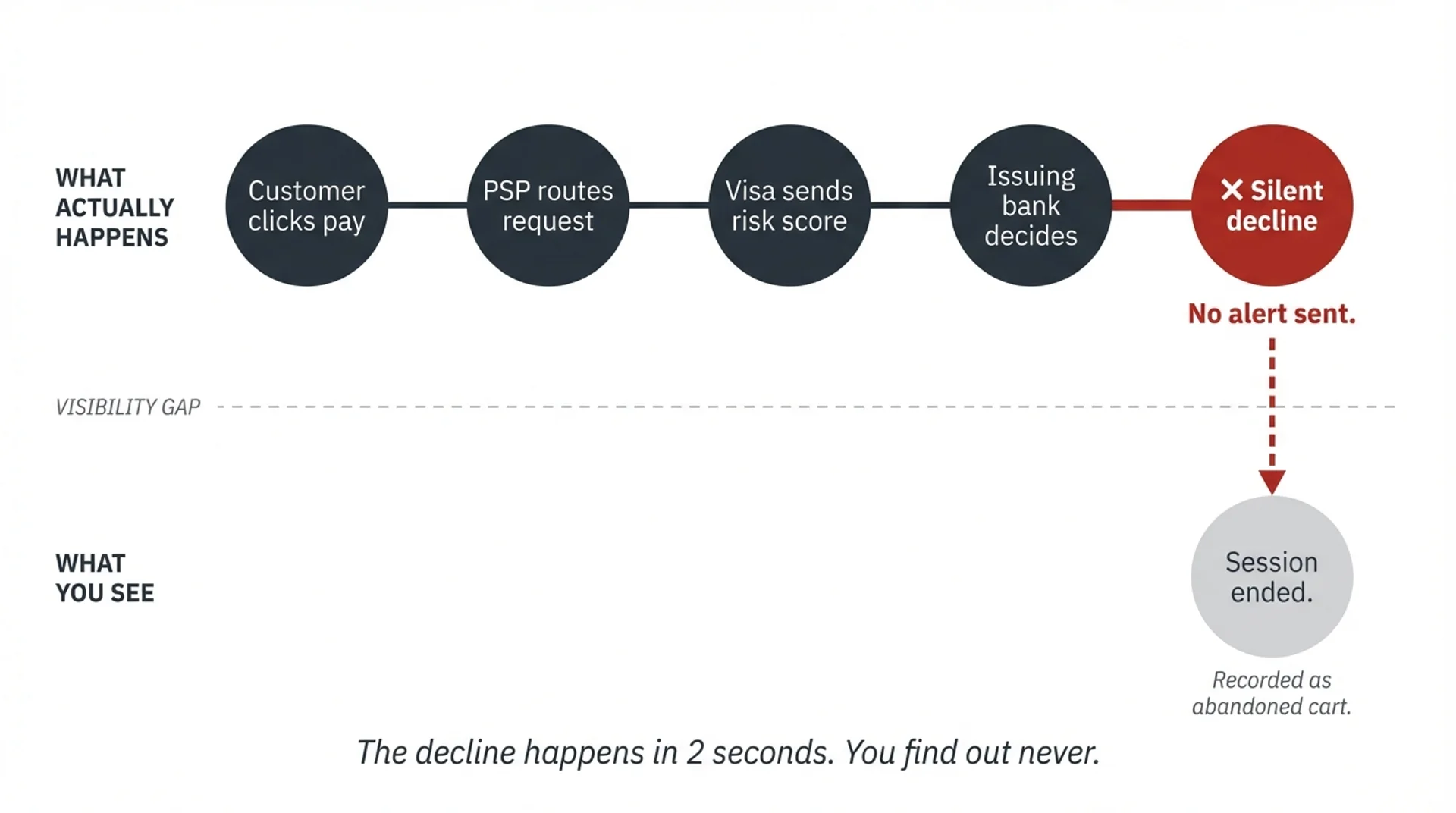

When a customer clicks pay, a process begins that most merchants have never seen described. The payment request travels from your checkout to your PSP, which routes it through Visa or Mastercard's network to the customer's issuing bank, the bank that gave them their card. That bank then makes a decision.

The decision is not simply "does this customer have funds?" It is a risk assessment. Visa sends the issuing bank a score between 0 and 99, calculated in real time across multiple variables: the type of card, the transaction amount, the country of the customer, the Merchant Category Code associated with your business, and the risk profile of the acquiring bank your PSP uses to process payments on your behalf. A higher score is a higher recommendation to decline. The issuing bank makes the final call. This entire process takes approximately two seconds.

If the transaction is declined, your customer sees a generic error. "Payment not completed." "Try a different card." Sometimes nothing at all. They do not know why. You do not receive a reason code in any dashboard you use daily. Your analytics platform records the session as ended.

The refusal is invisible to both parties.

Why Geography Is the Hidden Variable

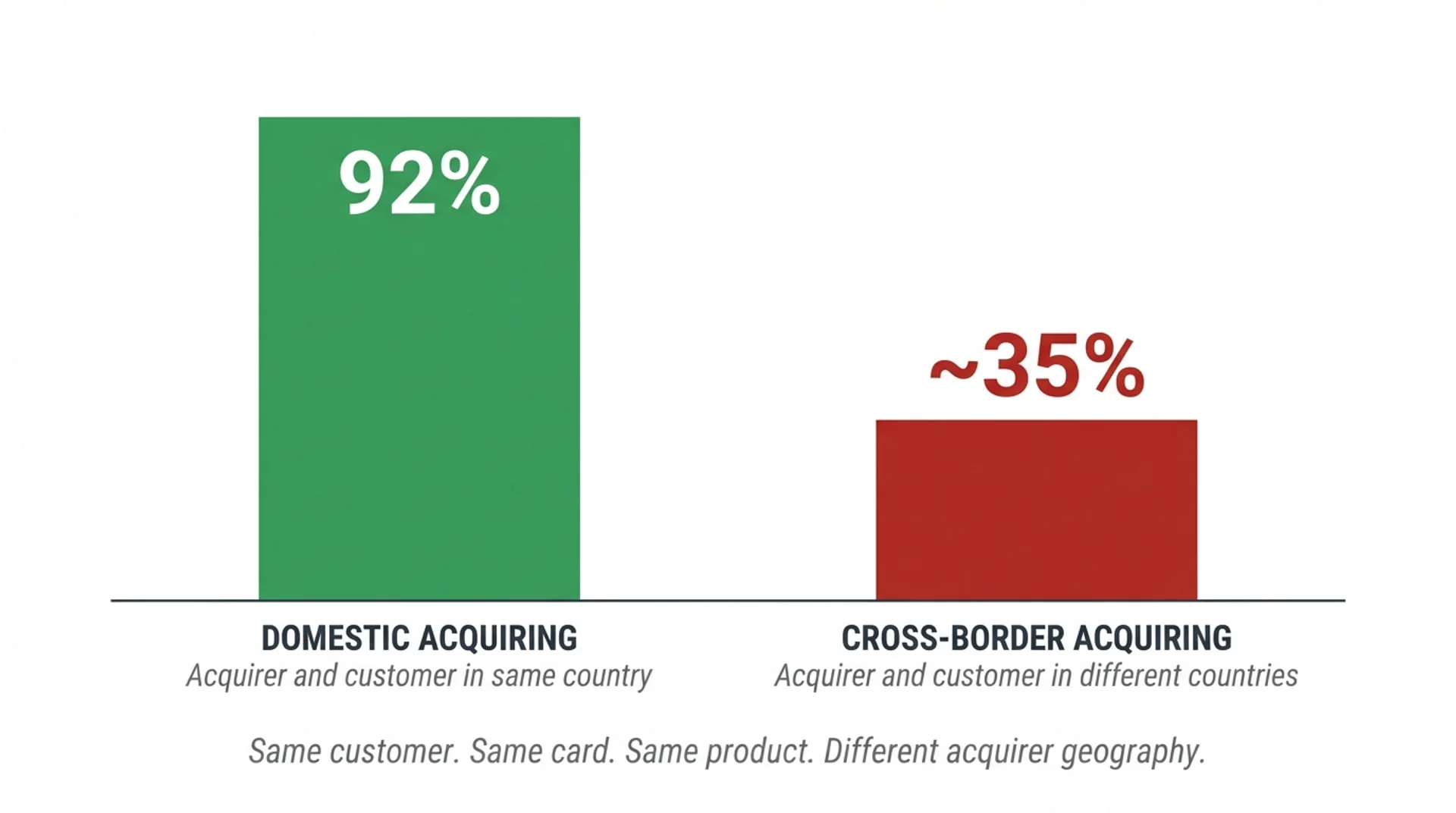

Authorization rates, the percentage of payment attempts that are approved, are not uniform. They vary significantly based on one factor that most merchants have no direct control over: the relationship between the country of their PSP’s bank and the country of their customer's bank.

When those two countries match, the transaction is treated as domestic. The customer bank's risk models are calibrated for domestic transactions. Approval rates are high, typically above 90%, often reaching 95% or more for standard card types.

When those two countries do not match, the transaction is classified as cross-border. The risk score Visa sends to the customer bank (issuing bank) is calculated differently. The issuing bank applies more conservative thresholds. And in markets where the PSP’s bank has no established local presence, Southeast Asia, Latin America, parts of Africa, the Middle East, authorization rates can fall dramatically. For merchants in certain categories or geographies, those rates can drop into the low double digits. That means fewer than one in five customers who attempt to pay successfully complete the transaction.

The other four see an error. You see an abandoned session.

The customers you are trying to recover with retargeting ads, email sequences, and abandoned cart flows are, in a meaningful percentage of cases, customers who never abandoned anything. Their payment was simply refused before they had the chance to complete it.

What This Looks Like in Your Numbers

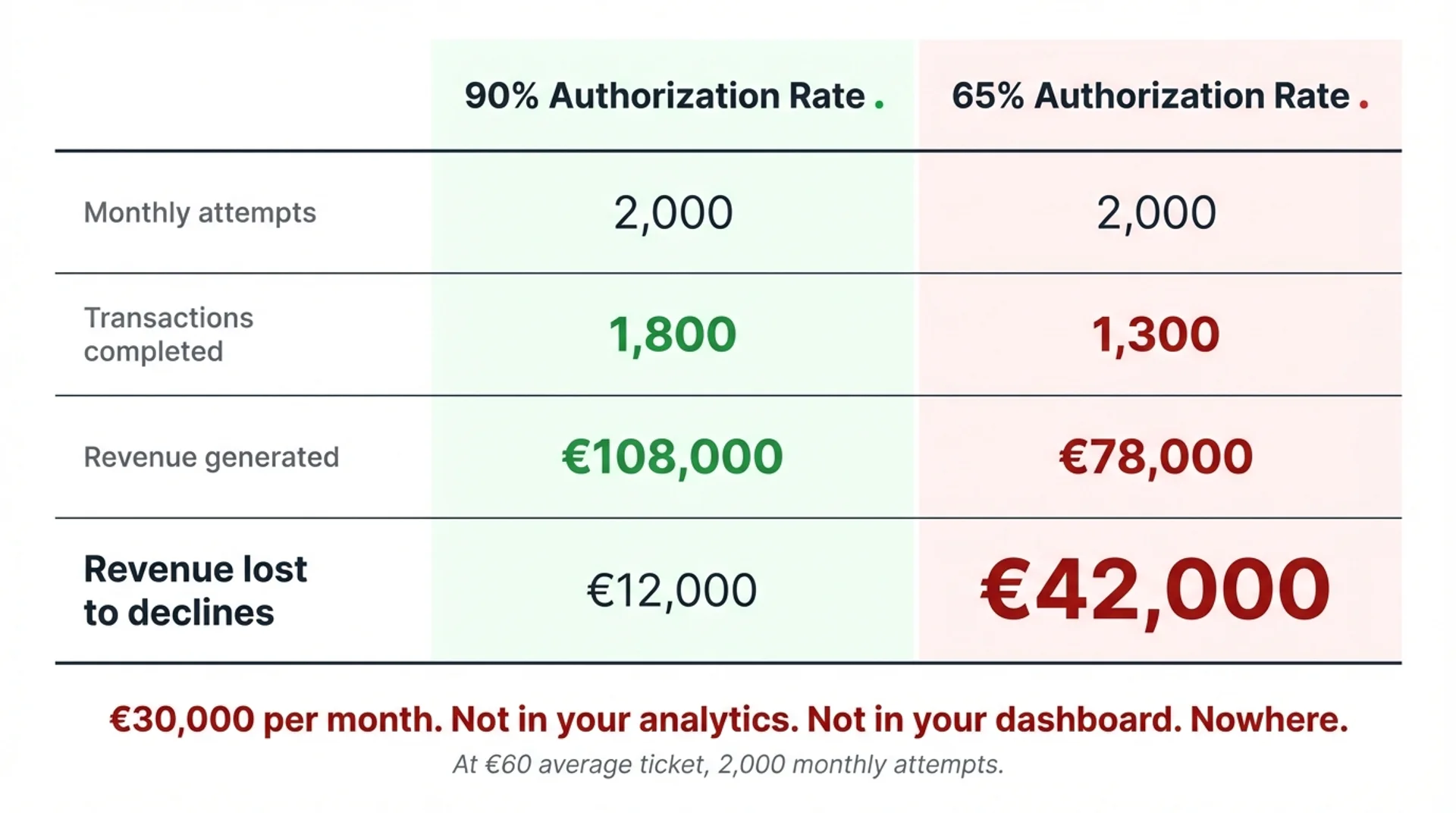

Consider a business processing 2,000 international payment attempts per month at an average ticket of €60. At a 90% authorization rate, standard for domestic processing, 1,800 transactions complete. At a 65% authorization rate, common for cross-border processing in certain markets, 1,300 complete. The difference is 500 transactions. €30,000 per month in revenue that does not appear in your PSP dashboard, does not appear in your Google Analytics, and does not appear in any report you review.

It does not appear anywhere, because from the perspective of every tool you use, those 500 transactions were never attempted. The customers simply left.

The practical consequence is that you are optimizing a conversion rate that is measured against successful payment attempts, not total payment attempts. Your actual conversion rate, from intent to purchase, is lower than you think. And the gap is not recoverable through better copywriting or a simplified checkout. It is recoverable only by changing the infrastructure that processes the payment.

Why Your Current PSP Cannot Fix This

Stripe, Adyen, Mollie, and virtually every mainstream PSP are built around one or a small number of banks, typically based in the United States or Europe. When a customer in Thailand, Brazil, or Canada pays through one of these PSPs, their transaction is routed through an bank that has no local banking relationship in that market. The transaction is cross-border by default. The risk score is elevated. The authorization rate drops.

This is not a product failure. It is an architectural consequence. These PSPs were built for merchants selling to customers in the same region as their bank. As long as your customers largely match that geography, authorization rates are high and the problem is invisible. The moment your customer base extends beyond that local market, the gap opens, and it widens with every new market you enter.

The only structural solution to low authorization rates in a given market is local banking, having a contract with a PSP’s bank in the same country or region as your customer. When your PSP’s bank that allows your to process and the customer bank operate in the same market, the transaction is domestic. The risk profile changes. The score changes. The authorization rate recovers.

Local PSP’s banking, done the conventional way, requires a legal entity in each market, negotiate a contract with a local banking partner, deal with local taxes and then rappratiate the funds back to your main market while dealing with currency fluctuations and finally a compliance process that repeats indefinitely as you expand. For a business with customers in ten countries, that is ten parallel legal and operational projects. For most growing companies, it is not a realistic path.

The Infrastructure That Makes Local Acquiring Accessible

What changes the equation is a card banking infrastructure that is not anchored to a single geography. When a PSP can route transactions through local card banking relationships across multiple markets without requiring the merchant to establish local entities, the authorization rate problem becomes solvable at scale.

This is the architecture Inflowpay was built around. Through a digital assets-based settlement layer, Inflowpay collects payments locally in each customer's market, via card, Open Banking, or local payment methods, and settles to the merchant account. The transaction is processed domestically in the customer's country. The risk profile is that of a domestic transaction. Authorization rates reflect local acquiring, not cross-border friction.

The result is not a marginal improvement in checkout conversion. It is a structural correction to a revenue gap that most merchants have never been able to measure, because the infrastructure they rely on does not show it to them.

If you sell to customers in more than one country and you have never audited your authorization rates by geography, the number you are optimizing is not the number that matters. The customers you are losing are not in your funnel. They are in a layer of your payment infrastructure you have never had reason to look at, until now.

You can see what your actual authorization rates look like with Inflowpay at inflowpay.com.