%20(1).png)

The most important stack in your business, and the one founders ignore the longest.

When people list the most valuable companies in the world, the same names come back: Apple, Google, Amazon, Coca-Cola, Microsoft. They all have one thing in common. They sell to consumers.

Conquering consumers is the holy grail. It is also, in the entrepreneurial world, the hardest thing to do. And when we talk about "hard", almost no one suspects that one of the most important steps of the sales cycle is hidden in plain sight: actually collecting the money. It looks like the easy part of the process. It is not.

It gets even worse when you remember that any serious company today wants to go global, and wants it fast. Patrick Collison once put it well: "Unlike more speculative paths to growth, optimizing your payments setup is almost guaranteed to yield extra revenue and to be among the highest-ROI growth activities you could undertake." He is right. Payments are the most under-optimized growth lever in most companies under $100M ARR.

This article is about that lever. We start from a real founder journey, then break down where the leakage happens, and finish with what you can actually do.

The journey every founder goes through

When you start out, you Google something like "payment gateway" or "how to accept payments online". The result depends on where you live. If you are Western and young, you land on Stripe. If you are older, you land on the Payment Service Provider your business bank pushed on you. In SEA you go to Xendit, in Africa to Paystack, in India to Razorpay, in Brazil to Pagar.me, etc. You don't really care. What you want is to charge customers. Everything else is not your problem. And honestly, at that stage, you are right.

You build a good product. You cross $1M ARR. 70% of your revenue comes from your home market, 30% from the rest of the world. You had never paid attention to that 30% before, but now you start thinking. The product seems to travel. Maybe it's time to double down internationally. You start dreaming of going global.

You don't change anything in your stack. You push into the US, the UK, the EU, Canada. It works. You scale. You hit $2M, then $5M, then $10M ARR.

Then you actually look at the numbers.

Each month, between 6% and 8% of your cross-border revenue is gone. At your scale that's $4K to $18K every month, evaporated for reasons you don't fully understand. You dig deeper into the transaction logs and you stumble on something else: a lot of declines. A lot. You panic, you Google, and you discover a notion you didn't know existed: acceptance rate.

You do the math. Over the last 12 months, somewhere between $100K and $500K in transactions were silently declined, with no obvious logic. Add it to the cross-border fees you're already bleeding and the number stops being a rounding error. It's a wound.

And then the rest of the iceberg shows up:

- You need to collect local taxes in every market and remit to every country.

- Chargebacks start spiking, especially when you launch a new geography.

- Some chargebacks are fraud. Some are customers who received the product and disputed anyway.

- Your fraud rules, tuned for your home market, instant-decline anything that looks "foreign", killing your acceptance rate further.

This is the moment most founders go down the rabbit hole. Three questions usually come up. Let's answer them.

1. Where do cross-border fees actually come from?

To answer that, we need to look at what happens when a card is tapped. The flow is the same everywhere on the planet, with small variations.

A customer pays $25 with their Visa card at a Square terminal. Six players are involved:

- Cardholder, the person paying.

- Issuing bank, the bank that gave the cardholder their card (e.g. TD).

- Merchant, the business getting paid.

- Acquirer (acquiring bank), the bank that processes payments on behalf of the merchant. Often, the Payment Service Provider (Square, Stripe, etc.) is also the acquirer or partners with one.

- Card network, Visa, Mastercard, etc. They route the message between the issuing and acquiring banks.

- Payment processor / POS, the tech layer.

When the card is tapped, the terminal grabs the PAN, expiry, CVV, and a one-time cryptogram from the chip. That data is wrapped into an ISO 8583 message (a 50-year-old standard, by the way) and sent over VisaNet to the issuing bank. The issuing bank checks balance, fraud risk, validity, then sends back an approval or a decline code (00 = approved, 05 = do not honor, 51 = insufficient funds, etc.). Visa relays the answer to the acquirer. The whole round trip takes about 2 seconds.

If approved, the issuing bank freezes the funds. At end of day, the acquirer batches all approved transactions and submits them to Visa for settlement. Visa runs a multilateral net settlement, instead of clearing every transaction one by one. It nets out flows between every pair of banks and produces a single net payment per pair. Settlement happens within 24 hours, 72 max, through a settlement bank (historically Chase Manhattan in New York for Visa). Banks true up via Fedwire or FedACH.

That sounds clean on paper. The fees, less so.

On a $25 transaction, a US merchant typically pays:

- Interchange fee to the issuing bank: 1.5% to +3.0%. This is the bulk of the cost. It funds card rewards programs. Visa sets the rates, but the issuing bank gets the money. Rates depend on card type (debit, corporate, rewards), Merchant Category Code (groceries cheaper than gambling), transaction type (chip cheaper than online), and ticket size.

- Network fee to Visa: 0.13% to 0.15%.

- Acquirer fee to Square/Stripe/etc.: 0.5% to 1.5% plus a flat fee per transaction.

Now, the kicker. Cross-border fees. The moment your transaction is "international", meaning the issuing bank country is different from the acquirer country, Visa and Mastercard add an extra layer:

- Cross-border assessment fee: roughly 0.6% to 1.0%

- International service assessment: roughly 0.4% to 0.8%

- FX margin from your acquirer: 1% to 2.5%

- Additional acquirer markup on cross-border: 0.5% to 1.5%

Stack it all up and on a cross-border card you are paying somewhere between 4% and 6.5% in total processing cost, vs. 2% to 3% for a domestic transaction. That gap is the cross-border tax that nobody talks about and that everyone pays.

Let's put numbers on it. Assume your blended cross-border overhead is 3.5% above your domestic baseline (a conservative middle of the range above), and that the share of revenue going through cross-border rails is 30%.

Now compound it. If you save that money and reinvest it at a modest 5% annual return, here is what the cumulative gain looks like over 5 years:

At $100M ARR, ignoring your payments stack costs you almost $6M of compounded value over 5 years. That's a Series A round you didn't need to raise.

2. What is acceptance rate, and why does it quietly kill you?

Acceptance rate is the percentage of your authorization attempts that get approved. If you push 1,000 charges and 850 get approved, you sit at 85%.

Founders think of acceptance rate as a binary, "the card works or it doesn't". It is not. It is the output of a probabilistic decision tree run in real time by the issuing bank. Here is what happens during those 2 seconds.

When the ISO 8583 message hits VisaNet, Visa runs the transaction through its risk engine and returns a score from 0 to 99 to the issuing bank. Higher score = higher recommendation to decline. The issuing bank takes that score, layers its own fraud model on top (account history, velocity, geolocation, BIN behavior, merchant reputation, etc.), and makes the final call.

The score is built on signals like:

- Mismatch between cardholder country and merchant country (cross-border = riskier)

- Merchant Category Code (some MCCs trigger automatic suspicion)

- Transaction amount vs. typical pattern

- Time of day, currency, AVS/CVV check results

- 3DS authentication status

- Acquirer reputation

- Historical chargeback ratio of the merchant, of the acquirer, of the BIN

A "good" acceptance rate depends entirely on your vertical and geography mix. As a rule of thumb, above 85% is healthy, above 90% is excellent, above 93% is exceptional.

And here is the counter-intuitive part: a too-high acceptance rate is a red flag, not a goal. If you sit at 99% on a cross-border vertical, you are either fronting fraudulent volume, or your fraud filters are off, and you are about to eat a chargeback wave that will blow up your processor relationship. The right target is "as high as possible while keeping chargebacks well under 0.5%". It's a ratio, not a max.

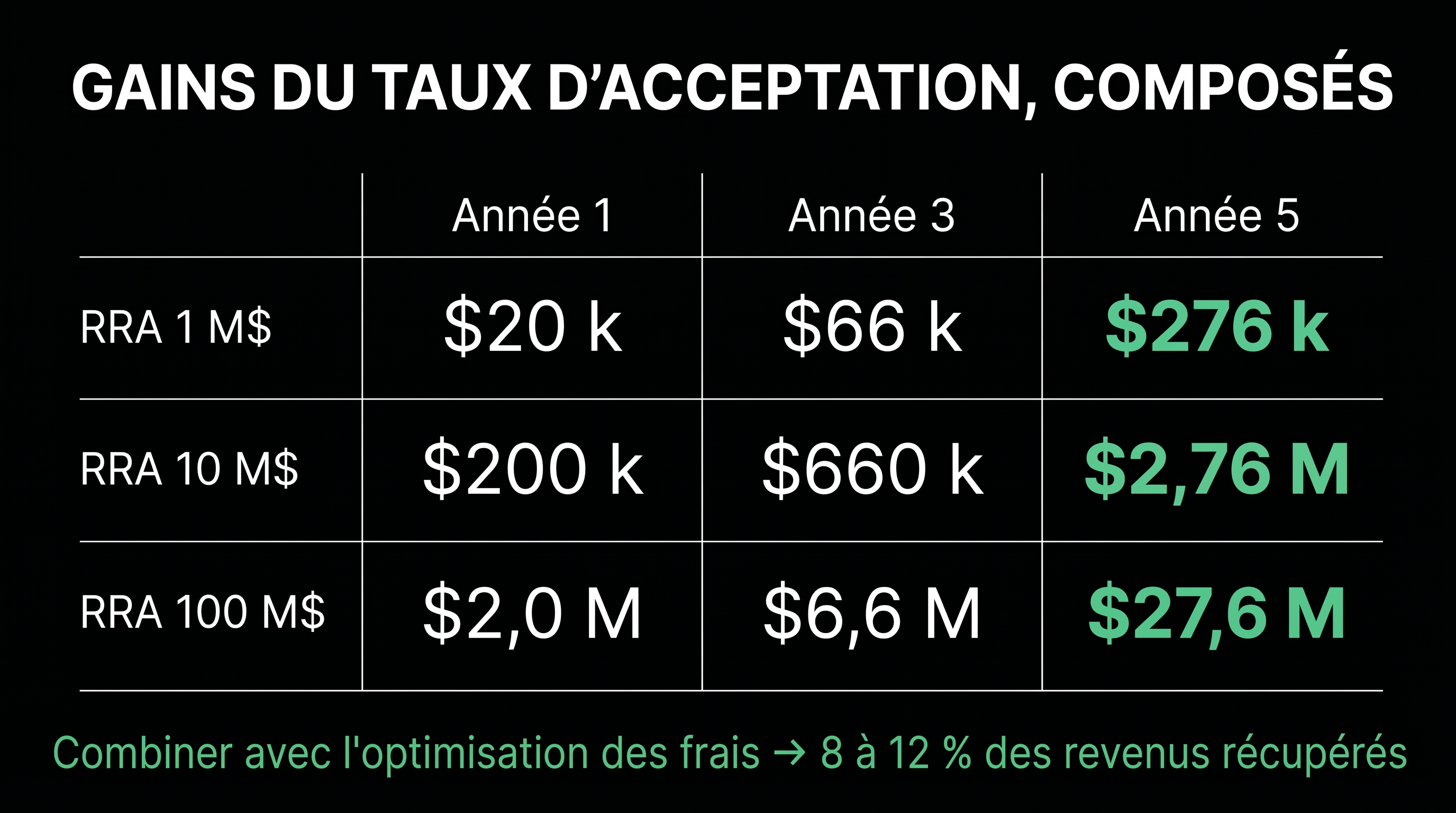

Why it matters financially. Let's assume you can recover 5 percentage points of acceptance rate with proper routing, retries, network tokens, 3DS optimization, BIN-level intelligence, and a payment stack that is actually built for cross-border. That is a realistic delta, not an aspirational one.

This is pure incremental revenue. You did the work to acquire those customers. The card was good. The money was there. The only reason it didn't land in your account is that the issuing bank's risk model, which was never tuned for your business, said no.

Compounded at 5% over 5 years, the same way:

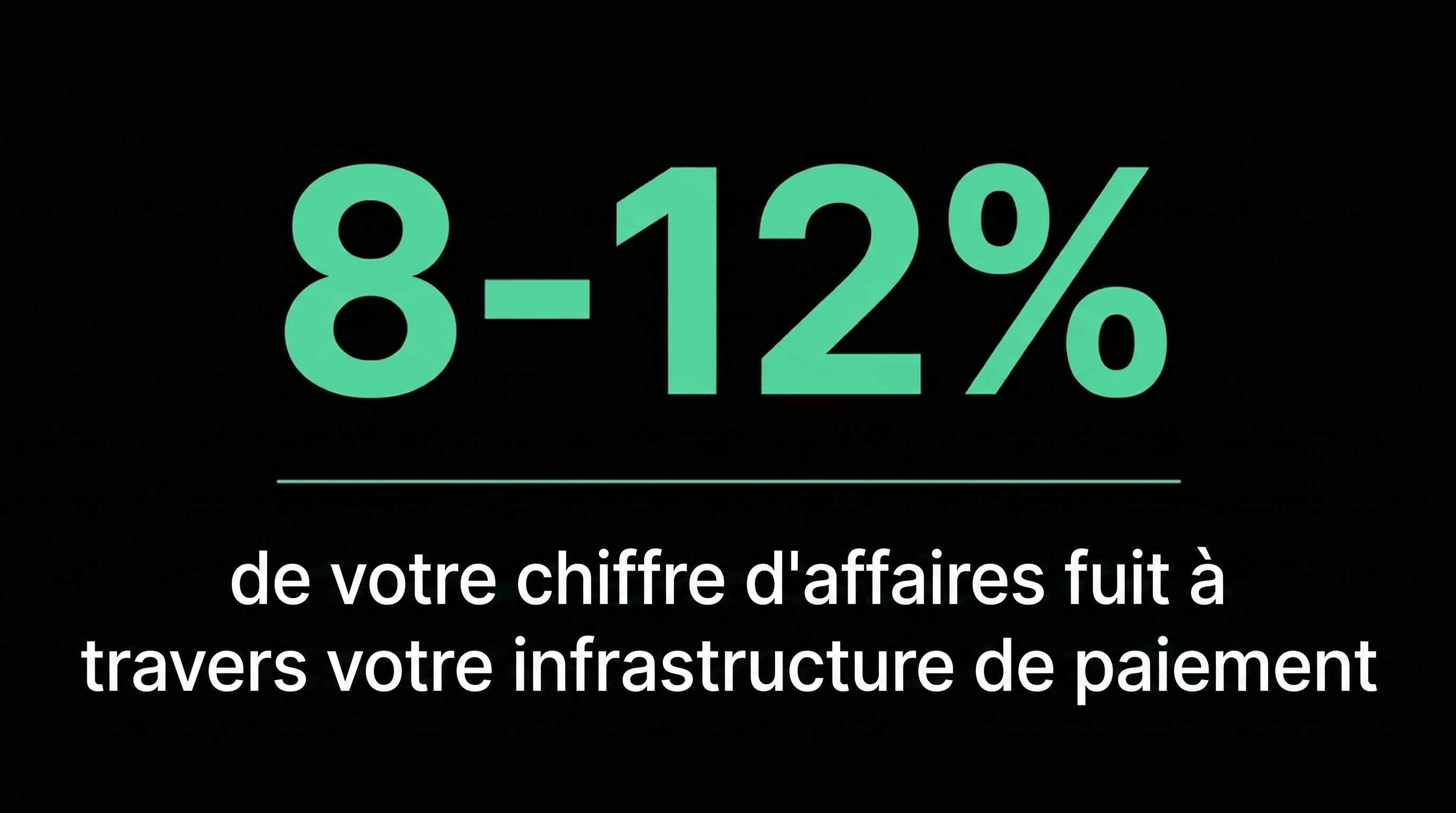

Combine cross-border fee optimization and acceptance rate optimization and you are looking at 8-12% of revenue you currently leave on the table in a typical cross-border-heavy SaaS or e-commerce business. At $10M ARR, that is the cost of three engineers you didn't need to hire.

The ironic part: this entire scoring system was designed for a world where the merchant was a brick-and-mortar store and the cardholder was physically present. Card-not-present transactions, cross-border digital goods, instant-fulfillment SaaS, marketplaces with sub-merchants, none of this fit the original model. The system is duct-taped on top of an old assumption. That is why the false positive rate is so high.

3. Chargebacks: what they are, why they will close your account, how to survive them

A chargeback is a forced reversal of a transaction by the issuing bank. It was introduced by the Fair Credit Billing Act of 1974 to protect consumers and increase trust in credit cards. Sixty years later, it is the single most underestimated risk in any merchant's life.

There are 3 main chargeback scenarios:

- Card present, chip transaction. When a customer pays IRL with a chip card, the merchant usually wins. Fraud loss is on the issuer.

- Card present, swipe. When the customer doesn't even have to chip the card, the merchant accepted the fraud liability and usually loses.

- Card not present (online). Liability is on the merchant by default. 3D Secure (3DS) shifts it to the issuer if used. US 3DS adoption was around 58% in 2024. Most merchants don't use it for friction reasons.

Now the part founders don't see coming. Chargebacks are not just a financial loss. They are an existential risk to your Payment Service Provider relationship.

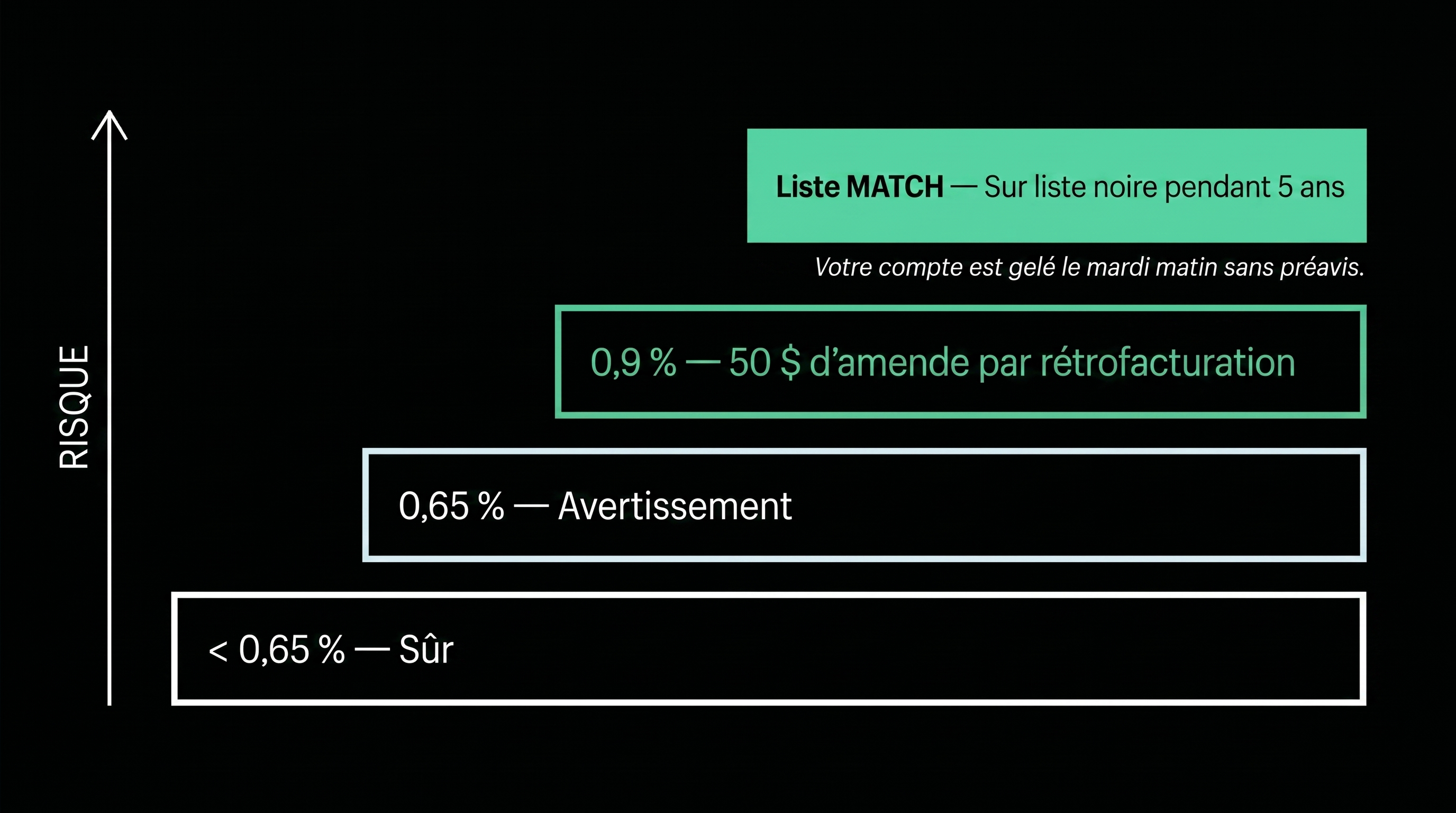

Here is why. When an acquirer sponsors you, they vouch for you to Visa. They legally promise that if you can't cover chargebacks, they will. So acquirers monitor your chargeback ratio obsessively. The thresholds Visa enforces:

- Below 0.65%: you're safe.

- 0.65%: warning.

- 0.9%: $50 fine per chargeback above threshold.

- 1.8%: $100 fine per chargeback above threshold.

If you stay in monitoring too long, fines escalate, and your acquirer gets charged $25K/month after 4 months, $50K/month after 7 months. Visa can mandate the acquirer to terminate you, or face suspension itself.

In reality, you will never even get close to those fines. Unless you are processing hundreds of millions of dollars per year, you are a small player to your Payment Service Provider, and they will take exactly zero risk on your behalf. At the first chargeback spike they don't understand, they cut you off. Better to lose a merchant than to risk their relationship with the network. The fines you read about are the upper bound. The real bound, for 99% of businesses, is "your account is frozen on Tuesday morning with no warning".

The cascade is brutal. You spike chargebacks. Your acquirer fines you. You get put on monitoring. You get terminated. You lose your processing capability overnight. You also get added to the MATCH list (Member Alert to Control High-Risk Merchants), which is essentially a blacklist shared across acquirers. Once you're on MATCH, getting a new processor is anywhere between very hard and impossible for 5 years.

I have seen this happen to companies doing $20M+ ARR. They didn't see it coming because nobody was monitoring chargeback ratio at the board level. By the time it was on the agenda, the account was already frozen.

How to actually manage this:

It depends on your vertical and your geographies. There is no universal playbook.

For certain verticals (marketplaces, server hosting, gaming, ...), chargeback management is a near full-time job. You need:

- Real-time chargeback monitoring (per BIN, per geography, per product, per acquisition channel).

- A fraud model that is updated weekly, because fraudsters adapt weekly. They use AI now. So should you.

- Un processus de représentation de contestation de paiement avec preuve de livraison, journaux IP, empreintes d'appareil, données 3DS, historique de communication.

- Systèmes d'alerte pré-contestation (Verifi CDRN, Ethoca) pour rembourser les litiges avant qu'ils ne deviennent des contestations de paiement.

Pour certaines zones géographiques, la stratégie est différente. Certains marchés (Brésil, Mexique, certaines parties de la région MENA) présentent structurellement plus de fraude car la culture de la contestation de paiement y est différente. La solution est rarement les filtres anti-fraude. Il s'agit de :

- Une communication produit et un processus d'intégration plus clairs pour réduire les remords de l'acheteur.

- Un support client localisé et réactif qui intercepte les demandes de remboursement avant qu'elles ne soient transmises à la banque émettrice.

- Des libellés de facturation adaptés pour que le client reconnaisse le prélèvement sur son relevé.

- Parfois des pré-autorisations ou une facturation échelonnée, pour offrir aux clients des fenêtres de désabonnement.

Être banni d'un Prestataire de Services de Paiement n'est pas une simple réprimande. Cela peut mettre fin à votre activité. Traitez le taux de contestation de paiement comme vous traitez le taux d'épuisement des fonds : un KPI au niveau du conseil d'administration.

Ce que vous pouvez réellement faire, par ordre de priorité

Si vous ne deviez retenir qu'une chose : les paiements ne sont pas une pile « à configurer et oublier ». C'est une surface d'optimisation continue qui s'amplifie. Chaque point de pourcentage que vous récupérez aujourd'hui est récurrent, à perpétuité.

La voie pragmatique, par ordre de ROI :

- Auditez votre relevé de frais, ligne par ligne. La plupart des fondateurs n'ont jamais fait cela. Vous y trouverez des frais transfrontaliers, des frais de conversion dynamique de devises, des frais de réseau et des majorations de Prestataire de Services de Paiement dont vous ignoriez l'existence.

- Mesurez votre taux d'acceptation par zone géographique, par BIN, par taille de transaction. Les chiffres agrégés masquent les fuites. Le schéma est presque toujours le même : 85-90 % dans le pays d'origine, 70-80 % à l'international, 50-60 % dans quelques BIN spécifiques que vous pouvez identifier.

- Mettez en œuvre des tentatives intelligentes. Une part significative des refus sont des refus temporaires (l'émetteur est temporairement incapable d'autoriser). Réessayer après 24 à 72 heures avec la bonne configuration permet de récupérer 10 à 20 % de ces transactions.

- Utilisez les jetons de réseau et le service de mise à jour de compte. Réduit les refus dus aux cartes expirées/remplacées. Gain gratuit.

- Ajoutez 3DS de manière stratégique. Pas sur chaque transaction. Uniquement sur les zones géographiques et les BIN à haut risque. Vous transférez la responsabilité sans nuire à la conversion.

- Pour les transactions transfrontalières, envisagez l'acquisition locale. L'acquisition locale supprime entièrement la pile de frais transfrontaliers et augmente votre taux d'acceptation. L'inconvénient est ce que cela implique réellement : créer une entité locale sur chaque marché, négocier avec un partenaire de paiement local, concilier une API différente pour chacun, rapatrier les fonds vers votre marché principal tout en gérant vous-même le change et les retards que cela engendre. Ce sont des heures de travail opérationnel chaque semaine, en plus d'une configuration qui prend des mois par zone géographique.

- Surveillez les contestations de paiement chaque semaine, pas chaque mois. Fixez des seuils internes (par exemple 0,4 %) bien en dessous de ceux de Visa. Au moment où vous atteignez le seuil de Visa, il est trop tard.

- Envisagez le routage multi-acquéreurs. Routez par montant, par secteur d'activité, par zone géographique, vers l'acquéreur le plus susceptible d'approuver. Le gain d'acceptation mentionné précédemment provient principalement de cela. L'inconvénient, encore une fois, est ce que cela implique : des mois de négociation avec chaque partenaire, et des minimums mensuels de plusieurs milliers par partenaire que vous payez que vous les utilisiez ou non.

La pile de paiement est le moteur à intérêts composés le plus sous-évalué de votre entreprise. Optimisez-la une fois, et elle vous rapporte à chaque transaction, pour toujours.

Si vous êtes une entreprise transfrontalière et que les chiffres ci-dessus vous semblent familiers, nous avons conçu Inflowpay pour résoudre précisément cet ensemble de problèmes :

- Frais — pas de cumul de taxes transfrontalières en plus de vos coûts de traitement. Ce que vous voyez est ce que vous payez.

- Taux d'acceptation — nous acheminons les transactions via plusieurs acquéreurs pour garantir un taux d'acceptation de +90 % sur chaque transaction.

- Fraude et contestations de paiement — nous les gérons pour vous, en nous appuyant sur des millions de points de données de notre base de marchands, afin que vous n'ayez pas à gérer une équipe de lutte contre la fraude.

- Rapatriement et change — nous rapatrions les fonds vers votre marché principal à des taux que vous n'avez jamais vus.

- Taxes locales — nous les collectons sur chaque marché et les reversons dans chaque pays pour vous.

Tout cela signifie que vous intégrez une seule API en moins d'une journée, et que vous n'avez jamais à embaucher une équipe de paiement et de fiscalité, à perdre des mois sur des configurations d'acquisition locale, ni à dépenser les centaines de milliers d'euros annuels nécessaires pour construire tout cela en interne. Nous gérons l'ensemble de la pile, vous vous concentrez sur votre produit.