%20(1).png)

You've been building toward it for months. A product launch that landed, a campaign that went viral, a promotion that converted beyond anything you'd modeled. The orders came in. The dashboard turned green. For the first time since you started this business, the numbers looked like what you imagined when you started.

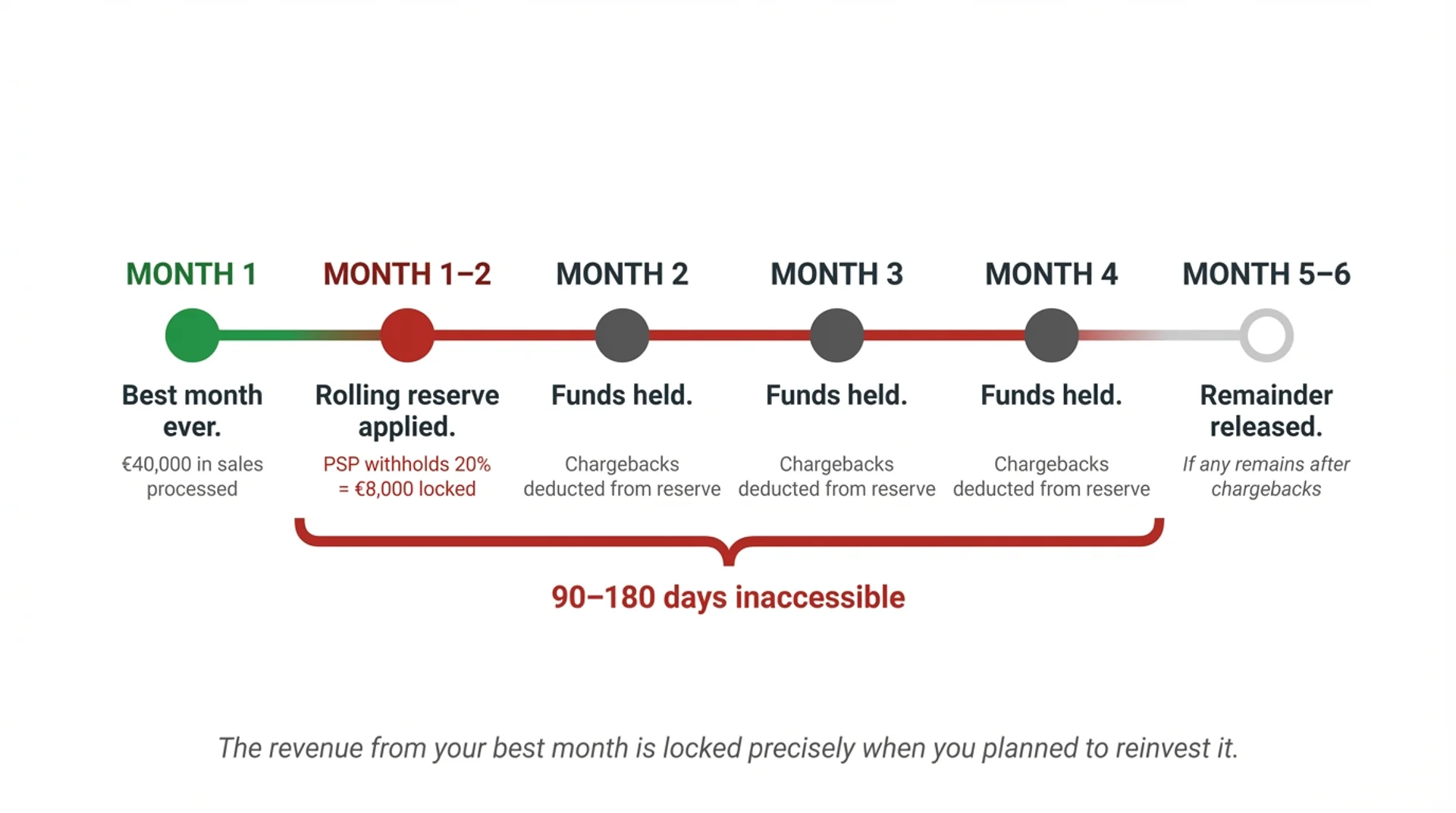

Then, a few weeks later, an email arrived. Your payment processing account has been suspended. Or a notification appeared in your dashboard: a rolling reserve has been applied to your account. Twenty percent of your future settlements will be held for ninety days.

You didn't do anything wrong. You had your best month. And that is precisely the problem.

What a Rolling Reserve Actually Is

Most merchants who sign up for Stripe, Adyen, or any mainstream PSP scroll past the terms and conditions without reading them. Buried in those terms, in the section on risk management, is a clause that grants the PSP the right to withhold a percentage of your settlement funds as a financial guarantee against future chargebacks. This is called a rolling reserve.

It works like this: your PSP takes a cut of every settlement, typically 5 to 20%, and holds it in a separate account for a defined period, often 90 to 180 days. The money is yours in theory. In practice it is inaccessible. If chargebacks occur during that window, they are paid from the reserve. Whatever remains after the period is released.

The rolling reserve is not a penalty. It is a mechanism your PSP uses to protect itself from the liability it accepted when it agreed to process payments on your behalf. You may never have known it existed until the day it was activated.

Why Growth Is the Trigger

Here is the part that most merchants never understand until it happens to them.

Chargeback ratios are percentages. But the amount at risk for the PSP that’s processing you are not. They are absolute numbers. And that distinction is everything.

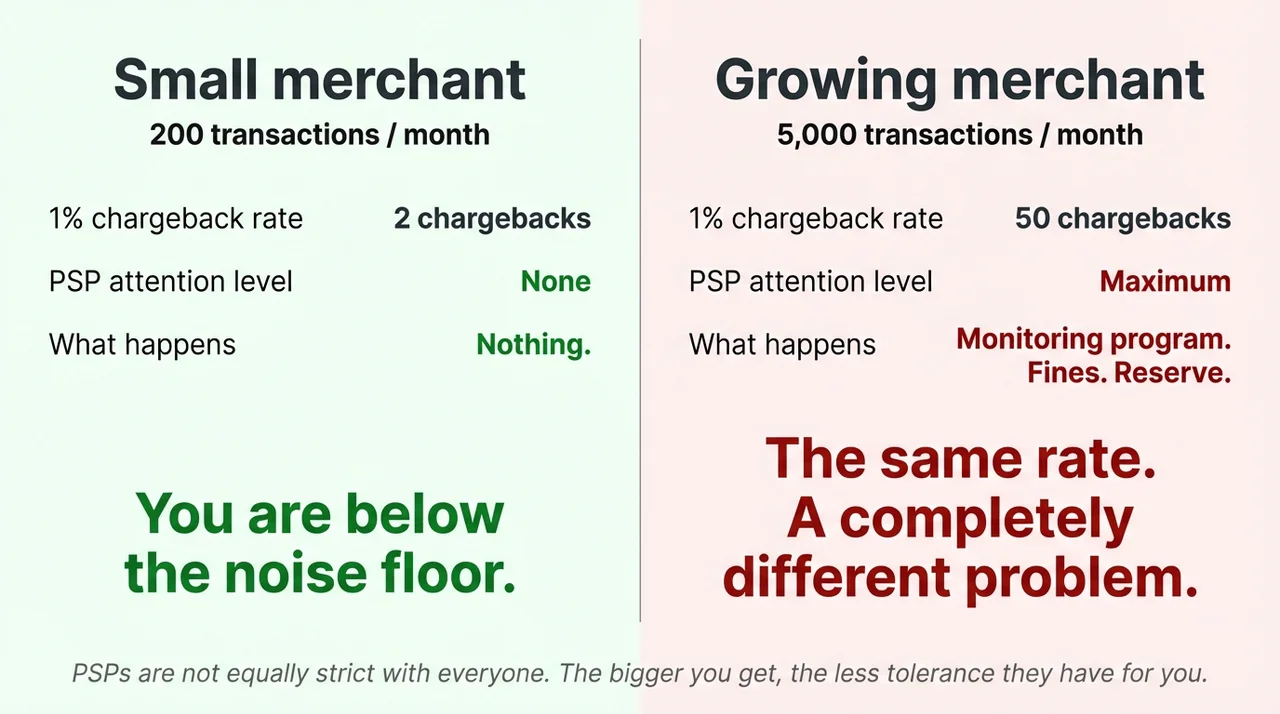

Say your average order is $100. At 200 transactions a month, a 1% chargeback rate means 2 disputes. Two customers out of two hundred asked their bank to reverse a $100 charge. Your PSP handles it quietly. You stay under the threshold. Nobody notices.

Now you run your best campaign ever. You hit 5,000 transactions in a month. Same product. Same price. Same 1% chargeback rate. That is now 50 customers disputing a $100 charge each. $5,000 in reversed transactions. And that number puts your account sur les radars, car la, le PSP, risque de perdre des montants qui ne deviennt plus négligeable pour lui.

The rate did not change. The amount at stake did

This is the dynamic most growing merchants never see coming. PSPs are not equally strict with everyone. When you are small, you are below the noise floor. When you scale, the same behavior that was invisible becomes a liability your PSP needs to manage. The bigger you get, the less tolerance the system has for you.

According to Mastercard, friendly fraud accounts for more than 45% of all chargebacks. Even with proof of delivery, cardholders win approximately 60% of disputes. Your best month brought in new customers. A normal percentage of those customers will dispute their purchase. At low volume, that percentage is invisible. At high volume, ca te met sur les radars de ton PSP

What Your PSP Sees

From your perspective, you grew. From your PSP's risk model's perspective, something else happened.

Your transaction volume spiked sharply and without gradual buildup. Your chargeback absolute count rose. You processed payments from geographies or card types you had not used before. And you did all of this without the historical track record that would allow the model to contextualize it as legitimate growth rather than a merchant running a short-term fraud scheme before disappearing.sur le t

Because that is what fraud schemes look like. A sharp spike in volume, a wave of chargebacks three to four weeks later when disputes are filed, and then silence. Your PSP's risk model was trained on both patterns. Yours and theirs are identical in the first thirty days.

The model does not know you. It knows the pattern. And the pattern is flagged.

You spent months building toward a breakout moment. Your PSP's risk infrastructure spent the same months optimizing for the day it would need to protect itself from exactly that kind of breakout.

The Account Termination Clause You Didn't Read

Beyond rolling reserves, there is a harder outcome. Stripe, Adyen, and virtually every mainstream PSP reserve the right to terminate merchant accounts immediately, without notice, if the account triggers certain risk thresholds. This is not a legal grey area, it is written explicitly in their merchant agreements. The conditions include chargeback ratios exceeding defined limits, sudden changes in processing volume, and undefined "suspicious activity" that the PSP determines at its sole discretion.

There is no appeal process. There is no grace period to bring your ratio back into compliance. There is no human at the PSP who reviews your account and considers context. The trigger fires and the account closes.

Support below $50 million in annual processing volume is functionally non-existent at most mainstream PSPs. There is no account manager to call. There is no escalation path. There is an automated system that evaluated your risk profile and made a decision, and a support ticket queue where the response time is measured in days.

The merchants who discover this are overwhelmingly merchants who did nothing wrong.

The Funds That Are Now Locked

When an account is closed or a rolling reserve is applied, the funds already in the settlement pipeline do not disappear. They are held. Sometimes for 90 days. Sometimes for 180. Sometimes longer if chargebacks continue to arrive against the reserve.

For a merchant who just had their best month, this means the revenue from that month, the cash they were planning to reinvest in inventory, ads, or headcount, is inaccessible at precisely the moment they had planned to use it. The growth that triggered the reserve is the growth they cannot now finance.

Why Your PSP Cannot Do Otherwise

The structural reason this happens is not that PSPs are indifferent to merchants. It is that they have no better tool.

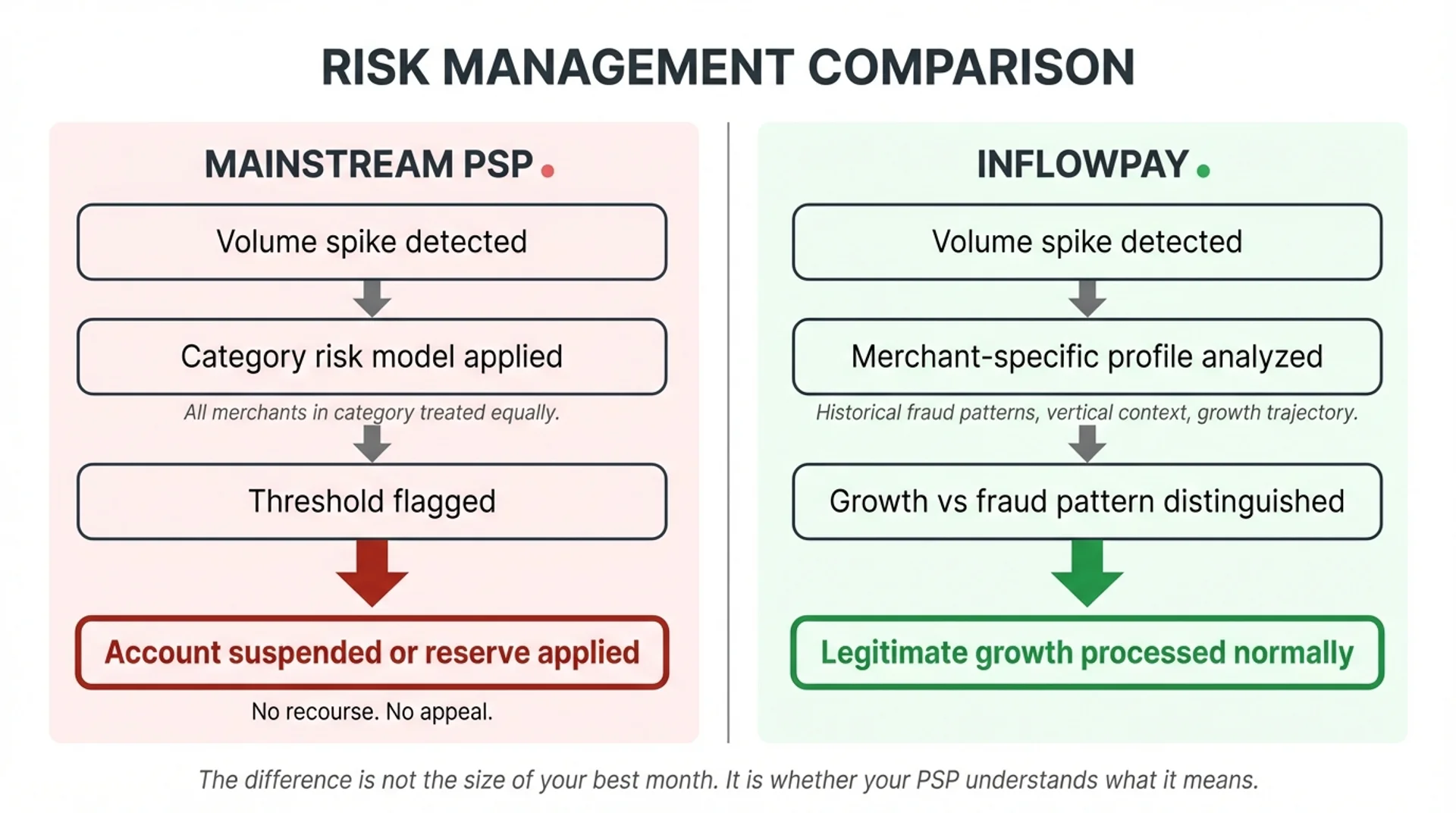

Risk at mainstream PSPs is underwritten by vertical and volume profile, not by individual merchant analysis. Below a certain processing threshold, the memo from Shopify Payments puts their account executive threshold at $60 million in annual processing, there is no human reviewing your specific fraud patterns, your specific customer base, or your specific growth trajectory. The automated system applies category-level risk models to your account. When those models flag you, they flag you as a category, not as an individual.

This is not negligence. It is the only economically viable approach when you are managing hundreds of thousands of merchants and cannot staff granular risk analysis at that scale. The fines Visa imposes on PSP are calibrated specifically to make tolerating risky merchants unprofitable. The PSP’s rational response is to eliminate risk before it materializes, not to investigate it after.

What Granular Underwriting Looks Like

The alternative to category-level risk management is merchant-level risk management, understanding the specific fraud profiles of specific verticals well enough to price and manage risk accurately at the individual merchant level rather than the category level.

This requires two things that most PSPs do not have. Fraud intelligence that compounds with every transaction processed, the longer you operate in a vertical, the better your models, the richer your data, and the more precisely you can distinguish a legitimate growth spike from a fraud pattern. And a risk assessment methodology that does not treat category as the primary signal.

Inflowpay collects datapoints that have been refined over years of operation and are constantly re-evaluated. Category is one input, not the driver. What this makes possible is a high-confidence read on whether a specific merchant is genuinely risky or not, independently of what vertical they operate in. Certain datapoints have proven to be cross-category predictors of fraud, reliable regardless of industry. Others sit at the individual level, signals tied to the person behind the business, not just the business itself, and these too hold predictive weight across verticals. The result is a risk assessment that looks fundamentally different from what mainstream PSPs produce. When your volume spikes, Inflowpay does not react. It investigates. It looks for context, asks questions, and makes a judgment. Rolling reserves and automatic blocks are responses to uncertainty. Granular data eliminates most of that uncertainty before a decision even needs to be made.

Your best month should be the beginning of a new baseline. Not the event that ends your payment processing. The difference between those two outcomes is not the size of your month. It is the infrastructure you are using when it arrives.

If you are scaling a business with international customers and you are processing through a PSP that has never spoken to you, the risk of your next best month is already present in your current setup. You can see what a different infrastructure looks like at inflowpay.com.