%20(1).png)

Last month, two of your customers bought the exact same product at the exact same price. One paid from Paris. The other paid from Bangkok. You charged them identically. You delivered identically. But what landed in your account was not identical, and the difference had nothing to do with your margins, your pricing, or anything you control. It had to do with six digits printed on a piece of plastic in Thailand.

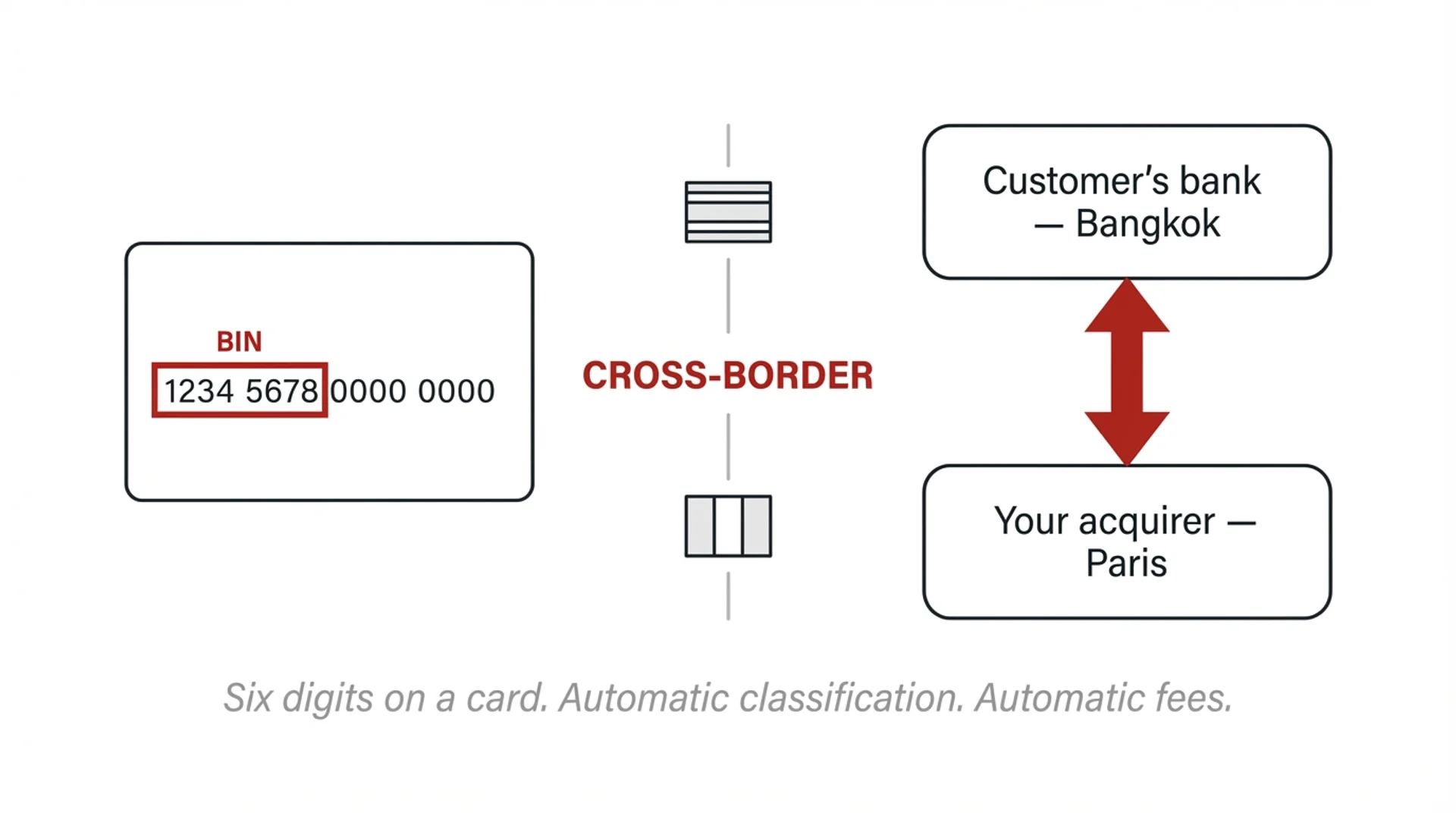

Those six digits are called a BIN, a Bank Identification Number. They identify the bank that issued your customer's card and, crucially, the country where that bank operates. When your customer in Bangkok tapped pay, Visa's network read those six digits, compared them to the country of your acquiring bank, and in a fraction of a second, classified the transaction as international. At that moment, a set of fees activated that had nothing to do with the size of the sale, the currency used, or whether the transaction was legitimate. They activated because your customer exists in the wrong country.

What Actually Happens When a Card Crosses a Border

The payment infrastructure that processes your sales was not designed to be neutral about geography. It was designed around a world where merchants sold domestically, to customers who shared a banking system with them. When that assumption breaks, which it does for virtually every business that sells online today, the system does not adapt. It charges.

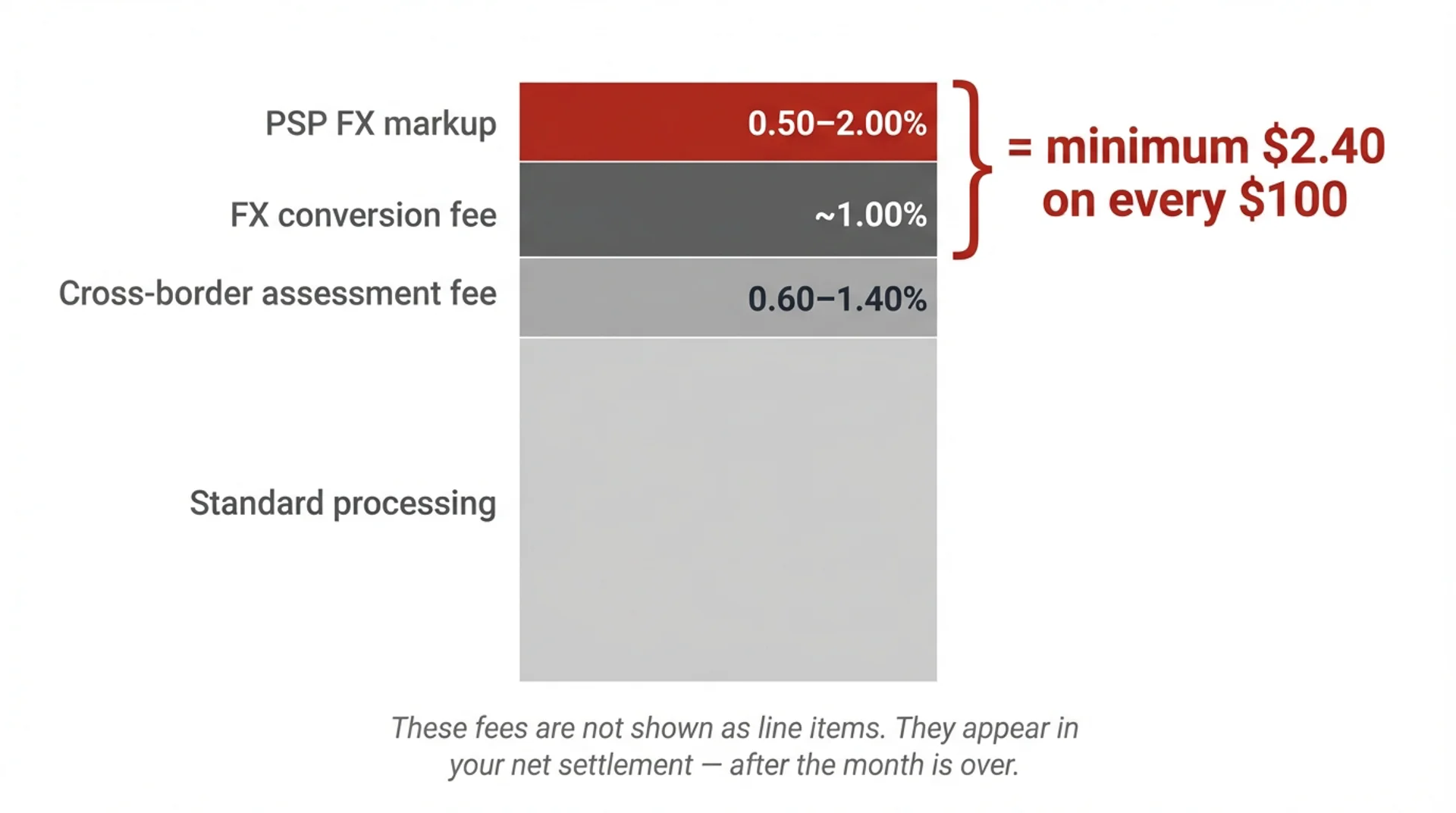

Here is what stacks invisibly on every transaction where your acquiring bank and your customer's bank are in different countries. Visa applies a cross-border assessment fee ranging from 0.60% to 1.40% depending on whether a currency conversion is involved. On top of that, if the transaction currency differs from your customer's billing currency, a foreign exchange conversion fee of approximately 1.00% is applied. Then your PSP or acquiring bank adds its own FX markup, typically between 0.50% and 2.00%. None of these fees appear as a line item your customer sees. None of them appear clearly on your dashboard. They surface only during monthly reconciliation, buried in a net settlement figure that is smaller than you expected.

On a $100 sale to an international card, the minimum cross-border cost is $2.40, before a single cent of standard interchange or PSP processing fees. On a subscription product with a $30 ticket, that same structure takes a percentage that starts to look less like a fee and more like a silent partner who does nothing and takes a cut of everything.

Every time a card issued in one country is used to pay a merchant in another, multiple invisible costs are triggered behind the scenes, often revealed only after the monthly reconciliation.

What makes this particularly difficult to diagnose is that cross-border classification is not triggered by the currency of the transaction. It is triggered by geography. A European customer paying in euros on your euro-priced website, using a card issued by a non-European bank, still generates a cross-border transaction. The currency never converted. The geography did the work. Even if the transaction is priced in USD, using a card issued in Europe can still trigger cross-border logic. The core determinant is always the same: BIN country versus acquirer country.

The Hidden Cost You Cannot See in Your Analytics

There is a second consequence of this classification that does not show up as a fee at all, it shows up as silence.

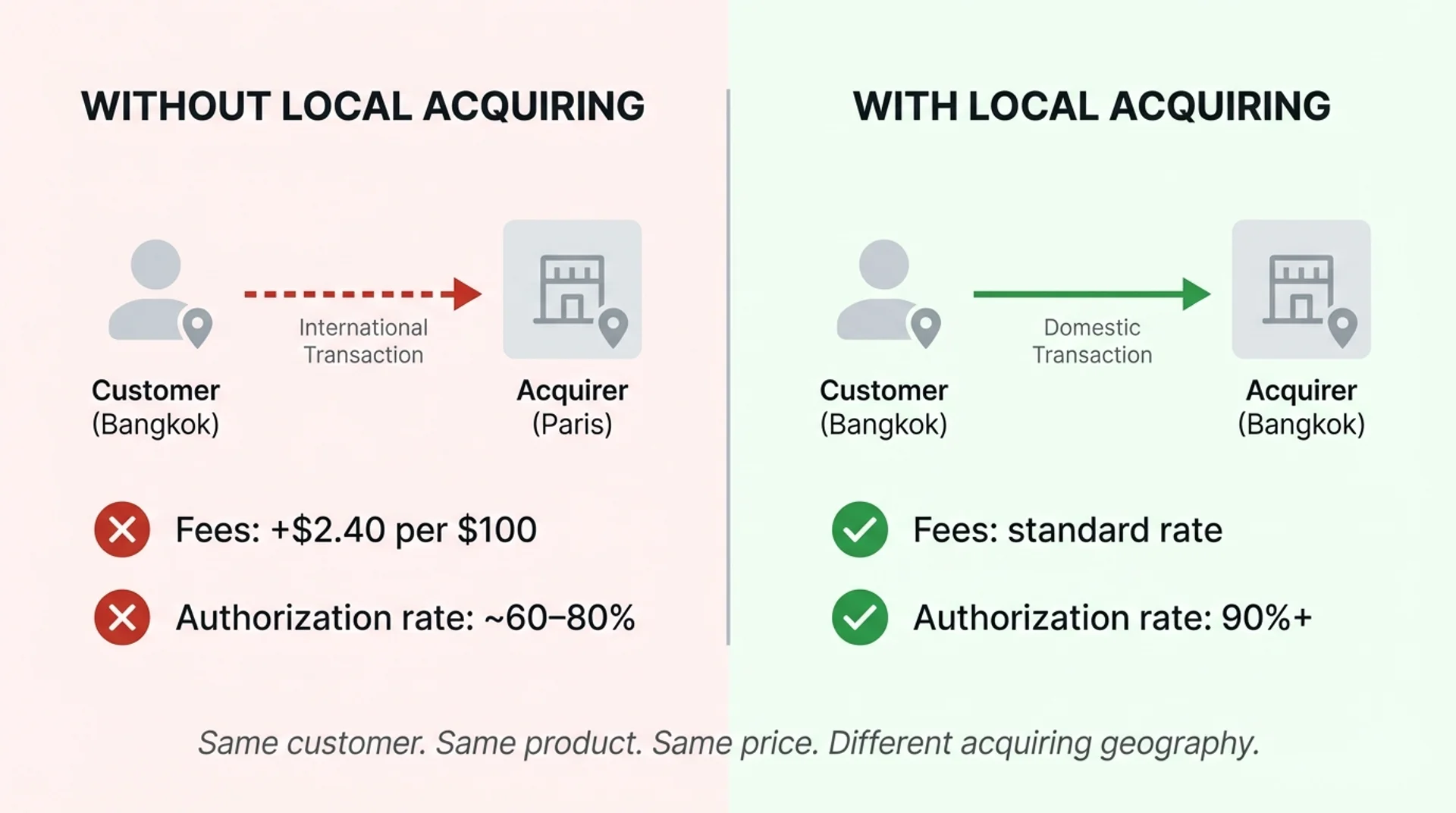

When your acquiring bank is in France and your customer is in Indonesia, the transaction is processed cross-border. Cross-border transactions carry lower authorization rates than domestic ones, because issuing banks apply more friction to international payments. Some of your customers in markets where your acquirer has no local presence are being declined. Not because they lack funds. Not because of fraud. Because the routing flags them as foreign, and the system applies a risk premium that results in a silent refusal.

Your checkout analytics show an abandoned cart. Your customer thinks their card was declined for a reason they don't understand. You see no error, no alert, no explanation. You attribute the drop to copywriting or UX. The real cause is that your acquiring setup was never built for the geography of your actual customers.

Why the Obvious Fix Is Structurally Inaccessible

The solution to cross-border fees and low authorization rates is called local acquiring, having an acquiring bank in the same country as your customers. When your acquirer and your customer's issuing bank operate in the same market, the transaction is domestic. Fees drop to standard rates. Authorization rates climb to 90% and above. The six digits on your customer's card stop mattering.

The problem is what local acquiring actually requires. To accept payments domestically in Thailand, you need a legal entity registered in Thailand, a local banking relationship, a separate compliance process with a Thai acquiring bank, and a mechanism to repatriate those funds back to your operating currency, typically via SWIFT, which costs between $15 and $45 per wire and takes days. Then you repeat this process for Indonesia, Brazil, India, the UAE, and every other market where your customers exist. There is no shortcut. There is no single agreement that unlocks all of them. Every country is its own legal and operational project.

This is why Stripe, Adyen, and virtually every mainstream PSP cannot actually solve this problem for you. They are domestically architected. Expanding to a new market means spinning up a new legal entity, repeating the full due diligence process, and rebuilding local acquiring from scratch, indefinitely, market by market. The majority of the globe remains structurally unreachable for a merchant using these tools, not because the PSP is negligent, but because their infrastructure was built for a different world. A world where you sold to customers who lived near you.

The Architecture That Changes the Equation

The businesses growing fastest today are not domestic by design. A two-person agency can have clients in 40 countries within months of launch. A digital product can reach a global audience the day it goes live. The old assumption, that cross-border commerce is an enterprise problem, solvable only by companies with legal teams and country managers, has collapsed. But the infrastructure most merchants are using has not caught up.

What changes the equation is not a different PSP doing the same thing more cheaply. It is an infrastructure that was built, from its foundation, to treat local acquiring as the default rather than the exception. The approach that makes this possible uses what payments teams call a stablecoin sandwich: collect in local currency, card, UPI, Pix, convert on-chain to a stablecoin at a fraction of a percent, and settle to the merchant. The result is that the transaction is processed locally, at local rates, with local authorization rates, without the merchant needing a single additional legal entity. The FX conversion happens on-chain at 3 to 10 basis points, compared to the 100 to 200 basis points charged by traditional banking rails.

This is not a workaround. It is a structural redesign of how acquiring works, one that makes the geography of your customer's bank irrelevant to the economics of your sale.

Thierry Bindini, an entrepreneur based in Mauritius working with clients across Europe, described what this shift felt like in practice. Between bank fees on every transaction and the complications of cross-border invoicing, he was losing money simply getting paid. Since switching infrastructure, in his words, the difference was not incremental, it was not even the same ballpark.

What This Means for You

If you sell to customers in more than one country, and if you are reading this, you almost certainly do, a portion of your revenue is being silently taxed every month by a classification system you never agreed to and probably did not know existed. Another portion is being lost to silent declines that show up in your analytics as abandonment rather than refusals.

Neither of these costs requires a legal change, a new product feature, or a negotiation with Visa to fix. They require a different acquiring architecture, one built for the world your customers already live in, not the world the payments industry was designed for.

Inflowpay was built specifically for this problem. Merchants using Inflowpay process local transactions in their customers' markets without forming local entities, at FX rates that are a fraction of what traditional rails charge, with authorization rates that reflect domestic processing rather than cross-border friction. If you are currently absorbing the cost of your customers' geography without knowing it, you can find out what you are actually leaving on the table at inflowpay.com.